SECTION 1: Market overview

1.1 What have been the key trends in the M&A market in your jurisdiction over the past 12 months and what have been the most active sectors?

Compared to 2016, a robust year for the M&A market in Taiwan, M&A activities were relatively slow in 2017. However, there were still some significant transactions in different sectors. While 2016 was called "the technology M&A year", the M&A activities in 2017 covered different industries.

One of the notable transactions was the privatisation of TCC International Holdings (TCCI – previously listed on the Hong Kong Stock Exchange) by Taiwan Cement Corp through a scheme of arrangement. For this privatisation, Taiwan Cement offered either cash or its shares to the other shareholders of TCCI. Taiwan Cement's operation in China would then be fully reflected in its financial performance as the result of the privatisation transaction.

Another major transaction was in the energy sector. Three of Taiwan's major solar cell and module manufacturers, Gintech Energy Corp, Neo Solar Power (NSP) and Solartech Energy announced in 2017 their plan to merge into one company and exit from the 'foundry' business model that they adopted, in order to form a solar flagship company with a competitive edge on the global market and vertical integration into the downstream solar system and power plant markets. NSP will be the surviving company after it merges with the other two companies, and the company after the merger will be renamed United Renewable Energy Co (URE). The transaction is expected to close in Q3 2018. With the blessing and capital support from the Taiwan Government in URE, this merger is deemed the Taiwan government's substantial effort on assisting the Taiwan clean energy industry players, in line with Taiwan's energy policy to abandon nuclear power by 2025.

As for the technology sector, in late 2017, Google announced the signing of a definitive agreement with Taiwanese smartphone maker HTC, to bolster its hardware business. Under the agreement, Google will acquire a team of HTC employees, many of whom have worked on its Pixel smartphone. In return, HTC will receive $1.1 billion in cash, and Google will also receive a non-exclusive license for HTC's intellectual property.

As for the financial sector, with the Taiwan government's "move south" campaign, Taiwan's financial institutions continued to expand their M&A activities in offshore markets; for example, Cathay United Bank and Cathay Life Insurance jointly acquired the Malaysian branch of the Bank of Nova Scotia Berhad; while China Trust Financial Holding Company invested in Thailand LH Financial Group Public Company Limited.

1.2 What M&A deal flow has your market experienced and how does this compare to previous years?

There were fewer M&A transactions in 2017 than in 2016 and the total value of the transactions decreased a few billion dollars. According to Bloomberg's M&A Legal League Table Rankings, the total value of announced transactions in 2016 was $23.8 billion with a deal count of 241, while the total value of announced transactions in 2017 was $17.13 billion, with a deal count of 202.

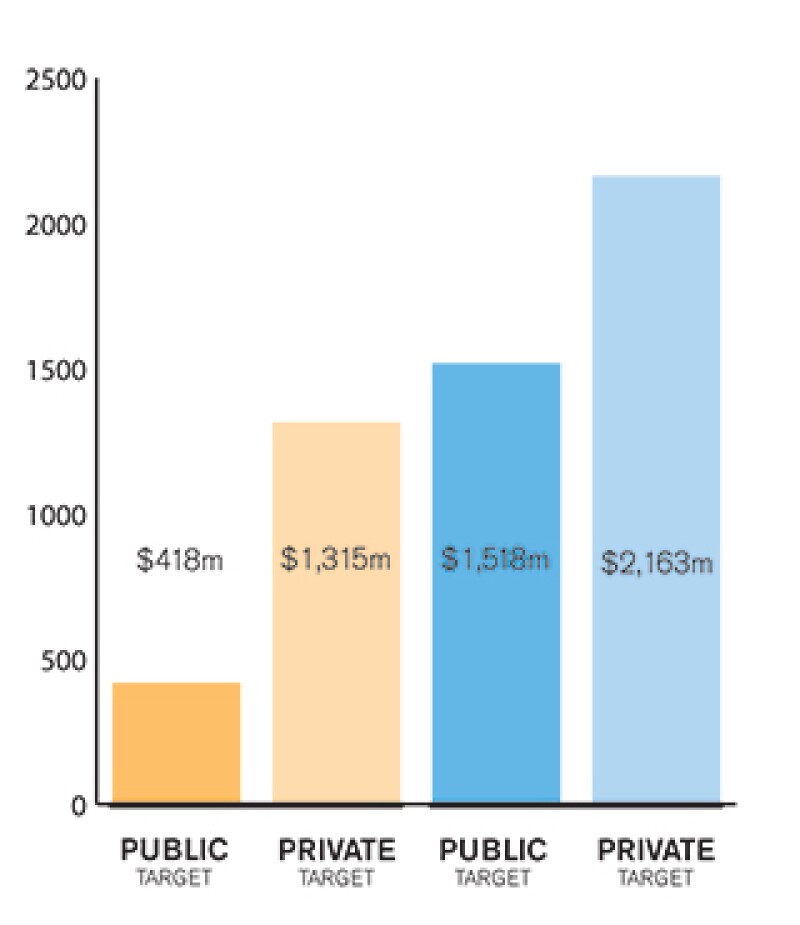

1.3 Is your market driven by private or public M&A transactions, or both? What are the dynamics between the two?

Both private and public M&A transactions are the driving force of the M&A market in Taiwan. While there were some notable public M&A transactions in 2016 and 2017, there have been quite a few private M&A transactions in the market as well. For example, there have been several acquisitions in the media industry, such as system operators, and small M&As for emerging technology companies. There were fewer investments by PRC/PRC-invested companies in Taiwanese companies through M&A due to the change of political climate and the sensitive cross-strait situation.

1.4 Describe the relative influence of strategic and financial investors on the M&A environment in your market.

Major M&A in Taiwan are mostly driven by strategic investors, such as the Gintech-NSP- Solartech merger for the energy sector, Google's acquisition of R&D team of HTC, and privatisation of TCC International Holdings by Taiwan Cement. Financial investors will usually participate in M&As as co-investors or acquire a minority stake of a company.

SECTION 2: M&A structures

2.1 Please review some recent notable M&A transactions in your market and outline any interesting aspects in their structures and what they mean for the market.

The three-in-one merger of Gintech, NSP and Solartech Energy, followed the traditional "merger" route under the M&A Act, whereby NSP will be the surviving company while Ginteck and Solartech will dissolve on the merger record date. As all three companies are listed, Ginteck and Solartech Energy will delist on the merger record date.

The privatisation of TCC International Holdings. is the first cross-border delisting project in Taiwan with an option of offering different considerations. The transaction is structured as a scheme of arrangements under the Cayman Islands law, which is also not common to see in the Taiwan market.

2.2 What have been the most significant trends or factors impacting deal structures?

There have been several driving forces in the structuring of M&A deals in Taiwan. For example, given that the newly amended M&A Act in 2016 allows more flexibility in terms of the form of the consideration that an acquirer may offer to the shareholders of the target company, it should be easier for an acquirer to achieve the purpose of acquiring 100% equity interest in a target company. Meanwhile, given the sensitivity of PRC investments in Taiwan, acquirers and targets should also be spending more time on structuring their transactions to meet the local restrictions/requirements regarding PRC investment in Taiwan, as well as their M&A goals.

Furthermore, following the XPEC Incident, the authorities have increased the financial burden on tender offerors and thus from now on, a tender offeror of a public company may need to substantiate its financial plan much earlier than before. Due to the XPEC Incident, how to avoid a tender offer, to the extent possible, becomes one of the considerations for proposed buyers of public companies when structuring a public transaction. Nevertheless, we still saw a few tender offers in 2017.

SECTION 3: Legislation and policy changes

3.1 Describe the key legislation and regulatory bodies that govern M&A activity in your jurisdiction.

The main statutes governing M&A activities in Taiwan are the M&A Act, the Company Act, the Securities and Exchange Act and the Fair Trade Act. In addition, under the Securities and Exchange Act, a set of tender offer rules are prescribed to govern the tender offer of public companies. Other statutes may also be relevant; for example, the Labor Standards Act and the tax laws and regulations.

The main regulatory body in charge of public M&A transactions is the Securities Futures Bureau (SFB) of the Financial Supervisory Commission (FSC), the government agency in charge of public companies. The other relevant regulatory bodies include the Fair Trade Commission (FTC), the authority in charge of anti-trust clearance, and the Investment Commission (IC), the authority in charge of reviewing foreign investments. If the target holds any special licence, the authority in charge of such special licence may need to review the transaction.

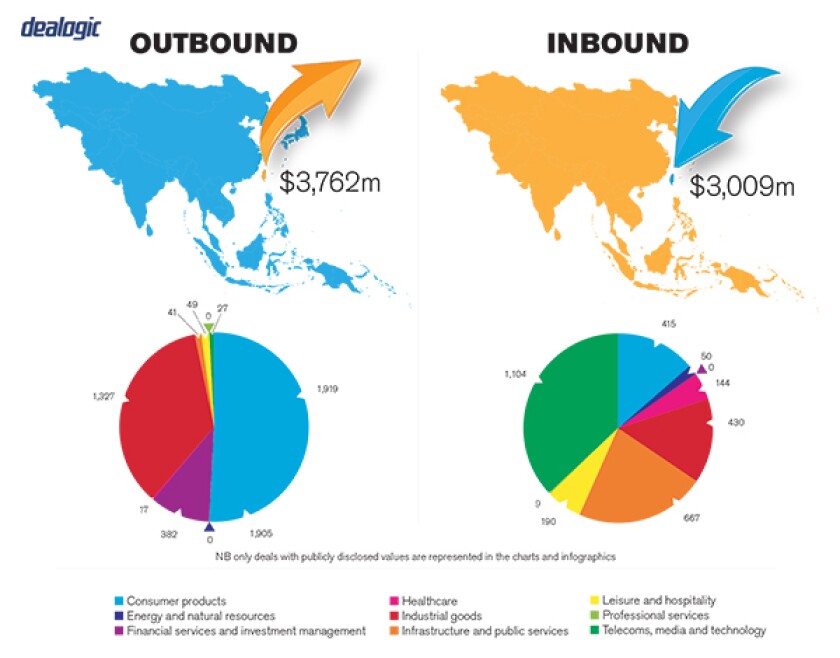

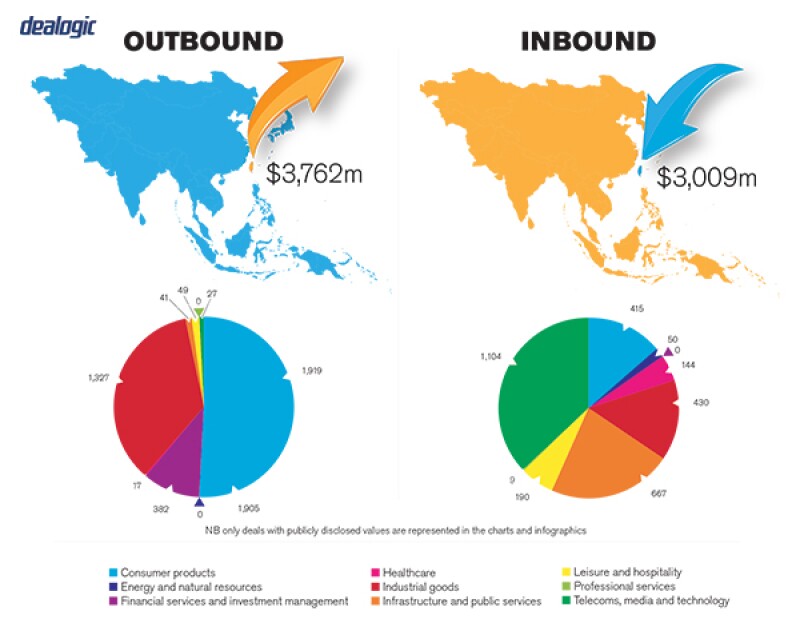

Inbound Outbound |

|

NB: Values may exclude certain transactions, for example asset acquisitions/sales |

3.2 Have there been any recent changes to regulations or regulators that may impact M&A transactions or activity and what impact do you expect them to have?

The 2016 amended M&A Act offers more flexibility in terms of the form of consideration that an acquirer is allowed to offer in statutory M&A transactions, such as share exchange. It also reinstates the possibility of structuring a triangular merger under the Taiwan legal system. In 2016, we saw the two largest public M&A transactions adopt the new cash-out share exchange to achieve the purpose of acquiring 100% equity interest in a public company. Thus far, we have yet come across a triangular merger.

Meanwhile, the tender offer rules were amended following the XPEC Incident. According to the amended Regulations Governing Tender Offers for Securities of Public Companies, a tender offeror is required to provide documents to prove its ability to settle the consideration stated in the tender offer. This means that a tender offeror may be required to have its acquisition fund in place at a much earlier stage of the tender offer.

Furthermore, the 2016 amendments to the Labor Standards Act caused tremendous controversy. The authorities therefore amended the Labor Standards Act again in January 2018, which will be implemented in March 2018. The change of holiday schedule, overtime payment, work days and work hours are key focuses of the authorities in protecting employees. As a result, when conducting a due diligence on the target company, the acquirer may need to pay more attention to such areas and carefully evaluate the relevant regulatory risks and contingent liabilities.

3.3 Are there any rules, legislation or policy frameworks under discussion that may impact M&A in your jurisdiction in the near future?

There are a few areas worth observing in this regard. First, with regard to the media industry, the government and the private sector are discussing whether to loosen the restrictions on government's and political parties' investment in companies operating TV channels or TV systems. Currently, the government and political parties are prohibited from investing in any TV channels or TV systems. As a result, many listed companies are prohibited from investing in such companies, given that government-operated funds would often times invest in listed companies by acquiring shares from the local market.

Meanwhile, PRC companies and PRC invested companies have been eager to invest in companies in Taiwan, such as semiconductor companies or online gaming companies. The current administration's position in this regard would determine whether and how such M&A transactions could be structured and proceed.

The government is also contemplating significant amendments to the Taiwan Company Act. Given that said Act may be amended to a great extent, future M&A activities may be impacted by such fundamental changes as well. However, the private sector has voiced strong objection against such amendments, and thus it may take some time for the government and the private sector to reach a consensus on whether and how the Company Act should be amended.

SECTION 4: Market idiosyncrasies

4.1 Please describe any common mistakes or misconceptions that exist about the M&A market in your jurisdiction.

Information disclosure and insider trading are important and sensitive areas for public companies. However, local management sometimes underestimates their importance and fails to make the proper disclosures. Large public M&A transactions, in many instances, crossed the red line as regards insider trading and quite a few criminal investigations have been launched. There have been many attempts to manipulate the stock prices of listed companies in order to reap improper gains. For example, with regard to the XPEC Incident, the chairman of XPEC was accused of assisting others to drive up the stock prices of XPEC via several avenues, including a proposed tender offer, so that they could gain greater profits from selling XPEC's shares on the market during the tender offer period.

4.2 Are there frequently asked questions or often overlooked areas from parties involved in an M&A transaction?

Information disclosure is an area to which public companies need to pay more attention when they plan M&A transactions. This would involve the proper information to be disclosed, as well as proper timing in disclosing certain information to the market. Most important of all, before proper information disclosure, the insiders in a public company should not trade any shares of the public company. Professional advice should be sought regarding this issue.

Another area that parties to an M&A transaction should pay more attention to is compliance with labour law requirements. As explained above, the Labor Standards Act was amended at the end of 2017, and the labour authorities have been strengthening the enforcement measures to further protect the rights and benefits of employees. Whether a target company is compliant with labour laws and whether there is any relevant contingent liability should be carefully assessed and ascertained.

4.3 What measures should be taken to best prepare for your market's idiosyncrasies?

In Taiwan, M&A transactions are often subject to regulatory approvals, such as foreign investment approvals or PRC investment approvals. For those industries that are required to hold special license/permit, such as banks, securities firms, insurance companies, and so on, the approval from the competent authority of such industries, such as the FSC, would need to be obtained in advance. Meanwhile, any M&A transaction triggering the pre-closing antitrust filing threshold would need to obtain antitrust clearance before closing. Given all these requirements, whether and how regulatory approvals can be smoothly obtained are issues critical to the completion of an M&A transaction in Taiwan. As such, it would be advisable for the investors intending to conduct an M&A transaction in Taiwan to seek professional assistance in advance, in order to better understand the required regulatory approvals and the application process involved.

SECTION 5(a): Public M&A

5.1 What are the key factors involved in obtaining control of a public company in your jurisdiction?

Given that under the Taiwan Company Act, material decisions would require the approval from shareholders holding two-thirds of the voting shares of a company, in order to gain an absolute control of a public company, an acquirer should aim to acquire or control at least 67% of the shares in a public company. In practice, given that not all of the shareholders attend shareholder meetings, to control the management or operation of a listed company, sometimes it is sufficient for one investor to control 30% to 40% of the voting rights in a listed company. In sum, this would largely depend on the shareholding structure of a particular listed company.

5.2 What conditions are usually attached to a public takeover offer?

In local practice, the conditions of a tender offer usually include the minimum and maximum number of shares that the shareholders of the target company shall agree to tender during the tender offer period; the tender offeror obtaining the required government approvals, if any (such as antitrust clearance and foreign investment approval, for example); and no occurrence of any material adverse event (subject to the approval of the FSC).

5.3 What are the current trends/market standards for break fees in public M&A in your jurisdiction?

In terms of tender offers and other types of M&A transactions between public companies, we have rarely seen break fee arrangements.

SECTION 5(b): Private M&A

5.4 What are the current trends with regard to consideration mechanisms including the use of locked box mechanisms, completion accounts, earn-outs and escrow?

The large private M&A transactions often adopt a completion accounts mechanism under which the purchase price is adjusted in accordance with the post-closing audit of the financial status of the target company as of the closing date. For transactions with a smaller value, it is more common for the parties to adopt the locked-box mechanism. The earn-out mechanism and escrow arrangements are commonly seen in private M&A transactions.

5.5 What conditions are usually attached to a private takeover offer?

The customary closing conditions attached to a private takeover offer usually include, among others, that the seller's representations and warranties remain true and correct; that the required government approval (if any) has been obtained; that the required third party consent (if any) has been obtained; that no material adverse event has occurred; that no action or government order is seeking to deter or enjoin the proposed M&A transaction; and that other commercial arrangements required by the parties have been completed or achieved (this would usually be structured based on the due diligence findings).

5.6 Is it common practice to provide for a foreign governing law and/or jurisdiction in private M&A share purchase agreements?

In the event that any party in a private M&A transaction belongs to a foreign corporate group, such a party would normally require that the transaction documents be governed by the law of the foreign country where the headquarters of the foreign corporate group is located, and that any dispute arising from the transaction documents be resolved via the court of a foreign jurisdiction or an arbitration proceeding conducted outside of Taiwan. Local parties would normally accept such arrangements.

5.7 How common is warranty and indemnity insurance on private M&A transactions?

Warranty and indemnity (W&I) insurance seems to be a better way for the seller and buyer to allocate their respective risks in an M&A transaction. Although we have seen the concept being discussed in local M&A transactions, the actual implementation of such mechanism is rare.

5.8 Discuss the exit environment in your jurisdiction, including the market for IPOs, trade sales and sales to financial sponsors.

The IPO market in Taiwan is generally perceived to serve the purpose of fund-raising more than an exit, due to lock-up requirements, minimum shareholding requirements, and legal requirements and limitations for selling shares applied to major shareholders, directors and supervisors. For the major shareholders of a public company that wish to sell their shares to a potential buyer, a mandatory tender offer may be triggered if more than 20% of the shareholding will be transferred within 50 days. Consequently, major shareholders' exit in the open market may be treated as a trade sale. In recent years, due to the low PE ratio of the Taiwan stock market and the strong performance of other stock exchanges in Asia (such as Shanghai Stock Exchange), the Taiwan IPO market has been slow, which is another reason why major shareholders usually would not consider Taiwan IPO market as way of exit as priority.

On the other hand, trade sales or sales to financial sponsors have always been a major route for exit. Other than highly regulated industries (such as media or cable TV) or acquisitions involving PRC funding, there should be no substantial hurdle for an exit, albeit that the regulatory approval process may sometimes take long time. As for the highly regulated industries and investment involving PRC funding, the Taiwanese government has been criticised for the prolonged regulatory approval process and lack of transparency in its decision-making process.

SECTION 6: Outlook 2018

6.1 What are your predictions for the next 12 months in the M&A market and how do you expect legal practice to respond?

Due to the sensitivity of the cross-strait relationship and the current government administration's conservative attitude toward PRC investment in Taiwan, we do not expect major transactions involving PRC funding taking place in Taiwan. However, it is anticipated that there will be more inquiries regarding so-called VIE structures or other alternative structures to achieve collaboration between PRC investors and Taiwan companies.

Counsels will need to pay more attention in planning such cross-border M&A activities in terms of coordinating the legal requirements in different jurisdictions and, more importantly, whether and how the various required government approvals can be obtained.

About the author |

||

|

|

Robin Chang Partner, Lee and Li, Attorneys-At-Law Taipei, Taiwan T: +886 2 2183 2208 F: +886 2 2514 9841 Robin Chang is a partner at Lee and Li and the head of the firm's banking practice group. His practice focuses on banking, capital market, international finance and mergers & acquisitions. He is a member of the Taipei Bar Association. Chang advises major international commercial banks and investment banks on their operations in Taiwan. He also advised six local banks for their customers' investments in structured notes issued by Lehman Brothers entities. He has also been involved in many M&A transactions of financial institutions, including AIG's sale of 97.57% shares of Nan Shan Life Insurance Company Limited. |

About the author |

||

|

|

Patricia Lin Senior counsellor, Lee and Li, Attorneys-at-Law Taipei, Taiwan T: +886 2 2183 2235 F: +886 2 2514 9841 Patricia Lin is a senior counsellor at Lee and Li. Her practice focuses on banking, securities, capital market, financings (particularly, structured and aircraft financing) and mergers & acquisitions. Lin has assisted many international capital market offerings (DRs, ECBs and Formosa Bonds). Lin is an M&A expert in both general and highly regulated financial and telecom industries. She advised on the first PRC investment into the LED industry. |

About the author |

||

|

|

Ken-Ying Tseng Partner, Lee and Li, Attorneys-at-Law Taipei, Taiwan T: +886 2 2183 2179 F: +886 2 2713 3966 Ken-Ying Tseng currently heads Lee and Li's M&A practice group (non-financial sector). She received an LLM from Harvard Law School. Having advised on various forms of mergers and acquisitions, she is experienced in resolving both legal and commercial issues. She has assisted many multinational corporations, such as BASF, Henkel, Yahoo!, AT&T, Arrow, Bureau Veritas, Aleees, DIC, Sony, Micrel, NTT DoCoMo, Energy Absolute, Feima, Qualcomm and Olin, etc, in their M&A activities. Ken-Ying has been recognised as a Leading Lawyer in the M&A field by IFLR 1000 from 2014 to 2016 and by Asialaw in 2013, 2014, 2016 and 2017. |

About the author |

||

|

|

Lihuei Mao Partner, Lee and Li, Attorneys-At-Law Taipei, Taiwan T: +886 2 2183 2274 F: +886 2 2713 3966 Lihuei (Grace) Mao is a member of the Taiwan Bar Association as well as the New York State Bar Association, and her practice area includes corporate and investment, mergers and acquisitions, securities law, anti-trust law and labour law. Mao has advised many venture capitals clients, PE funds and international groups in different industries on investments of different stages, from early-stage and complex mergers and acquisitions to IPOs. Mao has extensive experience in advising PRC companies in evaluating and structuring their investments in Taiwan. Recently, she has been active in assisting foreign investors investing in renewable energy projects in Taiwan. Mao has been recognised as leading lawyer by Asialaw for many years. |