Ignacio Balañá and Iñigo Zumalabe, Deloitte Legal

MARKET OVERVIEW

Despite the apparent economic slowdown and the uncertainty of the macroeconomic environment, the Spanish M&A market experienced a positive 2018 and we therefore feel relatively optimistic about the market's appetite for 2019.

M&A activity

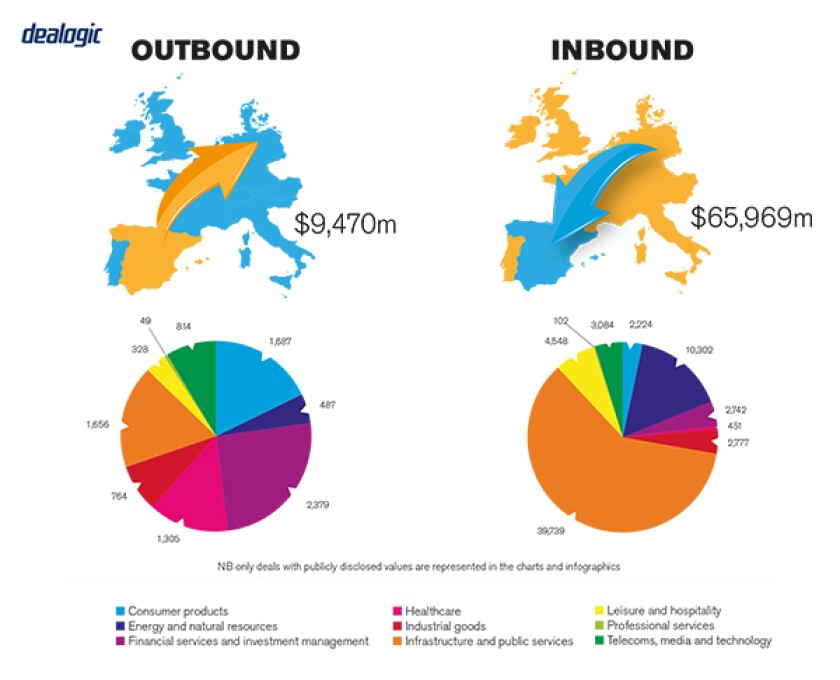

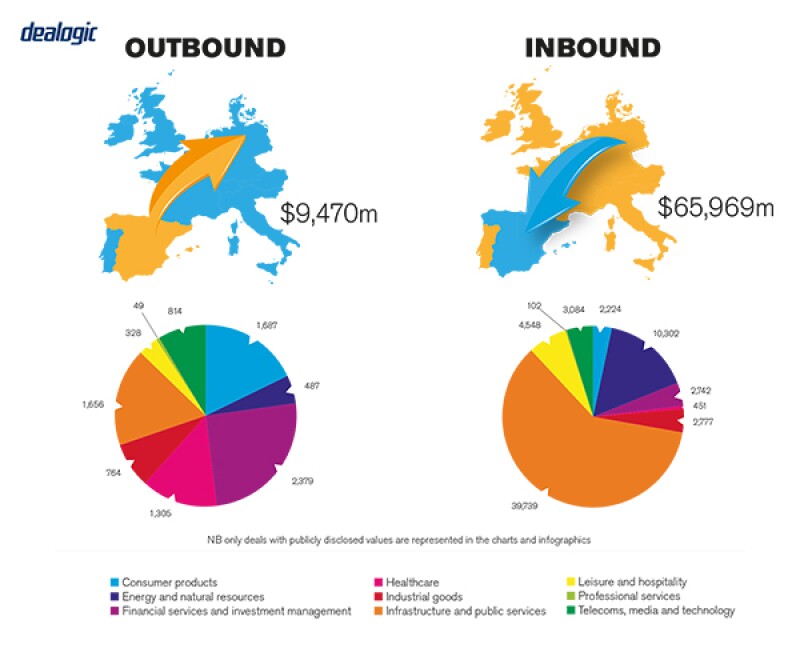

According to market analyst TTR, the number of M&A transactions closed in 2018 reached 2,454 and was 6% higher than in 2017, while the total value of the transactions was 19.04% larger (approximately €116 billion or $131 billion).

Besides the notable growth in the real estate and technology sectors, it is worth noting the strong entry of the healthcare sector among the most active sectors in terms of M&A transactions during 2018 (with a growth rate of approximately 103%).

It is normal for the Spanish market to observe both private and public M&A transactions. Although 24 IPOs were launched and successfully executed in 2018, some of them started back in 2017. Some highlight transactions were carried out in 2018 involving companies such as Abertis, Saeta, Europac, NH, Hispania or Testa. Clearly, public M&A transactions have been concentrated in the infrastructure and real estate sectors.

Given that the large amount of available liquidity, low price of credit and low market valuation of some listed groups are all expected to remain constant throughout 2019, it should come as no surprise to see more public M&A transactions over this year, although it cannot be totally disregarded that the volume may be slightly reduced.

TRANSACTION STRUCTURES

Interest from increasingly sophisticated foreign investors to enter the Spanish market or expand business activity in Spain has become more common and noticeable and this has resulted in the local M&A market maturing. The general decrease in transactions structured through open bidding processes has resulted in bilateral / one-to-one or limited competition processes (no more than two or three potential bidders) becoming ever more frequent.

Financial investors

Both strategic and financial investors have key roles in the Spanish M&A marketplace. Both large strategic investors such as ACS, Enagas or Amadeus or "usual suspects" in the private equity and venture capital arena are usually involved in the most relevant M&A transactions in Spain. Private equity big names are truly active in Spain (some of them having even opened physical offices, which suggests that their plans are to keep Spain on their radar).

Recent transactions

The acquisition by ACS and Atlantia of Abertis, the sale by Repsol of approximately 20% of the share capital of Gas Natural to CVC Capital Partners and the sale by Cinven of the Spanish business of Ufinet to Antin Infrastructure Partners were all key transactions in 2018.

The transactions were characterised for being highly competitive and challenging processes and for being related to infrastructure assets, pursuing the stability in the returns of the investment; and mature sectors and assets, but with positive upside for investors once restructured or refinanced.

In addition, most of the above target companies operate businesses outside Spain, which is an incentive for investors to access other territories such as Europe and Latin America and suggest that Spain remains as an excelent hub for investments in these geographical areas.

LEGISLATION AND POLICY CHANGES

Private M&A activity in Spain is mainly governed by the Spanish Civil Code; Spanish Commerce Code; Spanish Companies Act; Spanish Corporate Restructuring Act; Spanish Competition Act; and Spanish Income Tax Act.

Public M&A activity in Spain is mainly governed by the Spanish Public Takeover Act and Spanish Securities Market Act.

The main regulatory bodies governing M&A activity are the National Securities Market Commission (CNMV), National Markets and Competition Commission (CNMC), with regard competition and regulated sectorial matters and the Bank of Spain and General Directorate of Insurance and Pension Plans (DGS).

All the above, as amended and complemented by additional national, local and sectorial regulations, as the case may be.

Recent changes in law

The entry into force of the European General Data Protection Regulation (GDPR) in May 2018 (and its subsequent transposition into Spanish law) has resulted in investors having to consider an additional area of potential risk when investing in Spanish companies dealing with massive data, since non-compliance with the provisions may result in penalties of up to € 20 million or 4% of the company's turnover during the previous financial year.

In addition, as a consequence of the entry into force of a new European Directive applicable to tax intermediaries, tax advisors assessing cross-border transactions in Spain will have to communicate to the Spanish Tax Authority certain information on the cross-border mechanisms in which they are involved, provided that a number of requirements are met (following the trend created by the US through its "tax shelter disclosure" system or by the UK through its "disclosure of tax avoidance schemes" system).

Regulatory changes under discussion

Due to the current composition of the Spanish Parliament and its difficulties in reaching a majority required for the approval of new regulations, no significant changes are expected in the M&A regulatory framework.

However, the Spanish Government included in its proposal of Act approving the State Budget for 2019 certain tax measures which may have an impact on M&A transactions. Among these measures are the limitation of the exemption over the distribution of dividends and positive income derived from the transfer of securities representing the equity of resident and non-resident entities.

MARKET NORMS

No common misconceptions exist about the M&A market in Spain, due to Spanish corporate practice having firmly matured over the years.

However, the tight timelines to which transactions are subject impact on the seller's ability when it comes the time to preparing the due diligence exercise; in many occasions, virtual data rooms are not properly completed and uploaded at the kick-off date, which impairs the due diligence process and difficults the purchaser's valuation of the target.

Frequently overlooked areas

Frequently asked questions mainly relate to legal and tax related formalities for executing transactions, since, as opposed to Anglosaxon closing mechanics, there are a significant number of formalities to be accomplished for completion.

PUBLIC M&A

According to Spanish regulations, an entity or individual is considered to have obtained control over a listed company when it reaches a percentage of voting rights equal to or greater than 30% of the listed company's voting rights, either directly or as a result of indirect or supervened control (toma de control sobrevenida); or it has appointed a number of directors which, together with those already designated by such entity or individual in the past, represent more than half of the members of the listed company's board of directors within 24 months following the date of acquisition of the lowest percentage.

In these situations, the entity or individual which has obtained control of the listed company must launch a mandatory takeover bid where the price has to be fair and equitable to all the shareholders, holders of subscription rights and holders of convertible debentures of such listed company.

Conditions for a public takeover offer

The main conditions attached to a public takeover offer are (following the EU Directive):

The offeror must request authorisation from the CNMV and submit a prospectus and certain complementary documentation within a month following the date of the public announcement to launch the bid.

The offeror must make public and disseminate the offer within five business days following the date on which it obtains the authorisation from the CNMV.

The timeline of the process is highly regulated.

The board of directors of the target company must draft and make public a report regarding the suitability and repercussions of the takeover bid, abstaining to perform any action that may be harmful for the offer (duty of passivity or deber de pasividad).

Break fees

Break fees are widely used in public M&A transactions in Spain. The requirements for them to be approved are specifically foreseen in Spanish regulations applicable to competitive takeover bids (ie they must: be detailed in the prospectus; not be for an amount up to 1% of the total amount of the offer; only be agreed with the first offeror; and be approved by the board of directors of the target company based on a report issued by the target company's financial advisors).

Reverse break fees are uncommon in the Spanish M&A market.

PRIVATE M&A

As mentioned above, the increasing interest from foreign investors in the Spanish market has caused M&A transactions and consequently the price mechanisms used to become increasingly complex and sophisticated. In this regard, locked-box mechanisms are more common in deals driven by private equity or venture capital funds, while industrial investors usually prefer completion accounts mechanism.

Earn-outs and escrows remain common options for all kinds of investors to guarantee the seller's liability for a limited period of time. In addition, warranty and indemnity insurance policies are becoming increasingly popular under M&A transactions.

Conditions for a private takeover

Private takeovers are not subject to specific regulations under Spanish law and are therefore governed by the agreement between the parties. Auction processes are usually governed by process letters, which regulate all the stages of and schedule for a transaction, including the different phases and deadlines. The content of these kinds of letters is in line with international M&A practice.

Foreign governing

As a general principle, M&A transactions executed in Spain are subject to Spanish law and jurisdiction is entrusted to Spanish courts and tribunals, especially when industrial investors participate in the deal. Multijurisdictional transactions involving foreign and/or finance providers may be subject to non-Spanish law. However, it is increasingly common for parties to agree to submit the resolution of potential disputes to arbitration institutions, whether Spanish or international.

The exit environment

IPOs as an exit alternative are less common in the Spanish M&A practice due to the need to fulfill a large number of formalities, which usually slow down the exit process and the fact that the success of the exit depends on the appetite of the market at any single moment, and its success is therefore driven by the appetite of the market at any given moment.

Nonetheless, financial sponsors are inclined to conduct an exit through dual-track process when possible, and recent experience demonstrates that an IPO has been an option particularly for international private equity funds.

Other exit mechanisms, such as secondary buyouts, are widely used by financial sponsors to perform their divestment.

OUTLOOK

During 2019, the Spanish M&A market will continue to be influenced by macroeconomic factors such as the potential slowdown in the world economy, commercial instability, the final outcome of Brexit and any consequences from the politic unreliability of certain EU countries, all of which may limit the number and/or value of M&A transactions compared to 2018.

However, the availability of financing, the significant volume of dry powder in the hands of financial sponsors (which forces them to continue seeking opportunities to invest the capital) and the current pipeline of transactions in the Spanish market are some of the elements that could compensate the negative effect of the factors previously identified.

About the author |

||

|

|

Ignacio Balañá Partner, Deloitte Legal Madrid, Spain T: + 34 915 145 000 W: www2.deloitte.com/es/es/pages/legal/topics/legal Ignacio Balañá has been a partner in Deliotte Legal's corporate practice since 2017. Ignacio has extensive experience in corporate and commercial law, M&A and private equity. He has advised national and international groups on M&A, joint-ventures, cross-border transactions, corporate reorganisations, project finance and private equity transactions. Prior to joining Deloitte Legal, Ignacio was a partner at Latham & Watkins and Cuatrecasas. He was seconded to the New York office of Simpson Thacher & Bartlett from 2002-03. He is currently a professor of corporate law at the Universidad Pontificia Comillas – ICADE and frequent speaker at private equity and M&A forums. He has been recognised by Best Lawyers Corporate and M&A since 2015 and the Banking, Finance and Transactional Law Expert Guide for M&A since 2018. |

About the author |

||

|

|

Iñigo Zumalabe Director, Deloitte Legal Madrid, Spain T: + 34 915 145 000 W: www2.deloitte.com/es/es/pages/legal/topics/legal Iñigo Zumalabe joined Deloitte Legal in May 2017 as a director. Iñigo has extensive experience in M&A, private equity and restructuring transactions as well as joint-ventures and financing transactions. He is recommended by Best Lawyers. Prior to joining Deloitte Legal, he worked at Garrigues and Freshfields Bruckhaus Deringer. |