SECTION 1: Market overview

1.1 What have been the key trends in the M&A market in your jurisdiction over the past 12 months and what have been the most active sectors?

The Austrian M&A market has been growing continuously for the past few years. Same as in 2016, 2017 showed a constant number of transactions with a massive increase in transaction value. The most active sectors in 2017 were the real estate, technology and industry sectors. According to the Ernst & Young market analysis for 2017, of 345 transactions which took place in 2017, 86 concerned the real estate market followed by 76 transactions in technology and 60 in industry.

Another trend that has been going on for the last few years is the increasing interest among foreign investors to enter the Austrian market. Meanwhile more than one third of all deals with Austrian relevance concerned foreign investments in Austrian companies.

1.2 What M&A deal flow has your market experienced and how does this compare to previous years?

The number of M&A transactions completed on the Austrian market has been steadily increasing. In 2017, pursuant to the Ernst & Young market analysis for 2017, 345 transactions took place which corresponded approximately to the number of transactions completed in the year 2016. M&A deals in Austria reached an aggregate transaction value of €14.7 billion in 2017, which is an increase of 37 % as compared to 2016. This trend in significant increase in transaction volume has been continuing since 2016 where a 10-year high was reached with a transaction volume of €10.7 billion corresponding to an increase of 66.2 % compared to 2015.

1.3 Is your market driven by private or public M&A transactions, or both? What are the dynamics between the two?

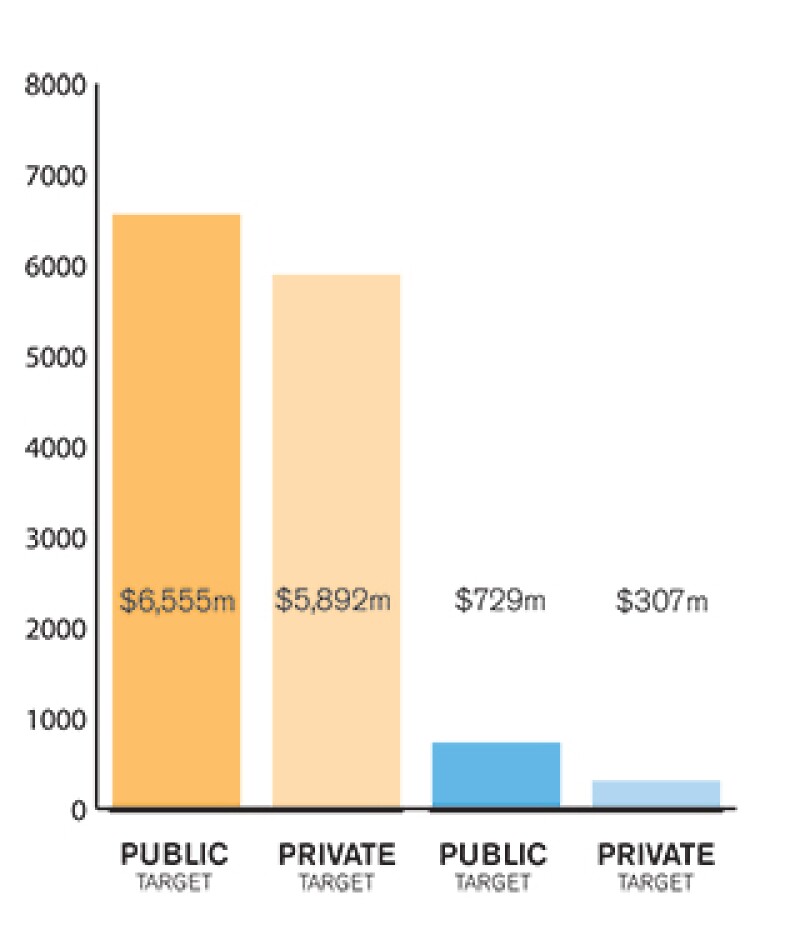

Most transactions on the Austrian market are private M&A transactions, whereas public M&A deals have not played a big role in the last few years. 2017 was, in this regard, an exception as the largest deal – the takeover of Buwog by Vonovia with a transaction value of €5.6 billion – was a public M&A transaction. However, the prevailing number of M&A transactions on the Austrian market are private.

1.4 Describe the relative influence of strategic and financial investors on the M&A environment in your market.

The influence of financial investors in the Austrian M&A environment is relatively slim. Only 20 out of 345 deals in 2017 were financial investments. On the other hand, strategic investments play a very large role on the Austrian M&A market. In 2017 the majority of transactions were performed by strategic investors.

SECTION 2: M&A structures

2.1 Please review some recent notable M&A transactions in your market and outline any interesting aspects in their structures and what they mean for the market.

2017 has seen four major transactions, which caused the aggregate transaction value of Austrian M&A transactions to increase significantly:

(i) The takeover of Buwog by Vonovia (transaction value of €5.6 billion);

(ii) The acquisition of UPC Austria by T-Mobile Austria (€1.9 billion);

(iii) The acquisition of the Russian gas field Juschno-Russkoje by OMV (€1.7 billion) and

(iv) The acquisition of the real estate portfolio of RFR Holding by Signa (€1.5 billion).

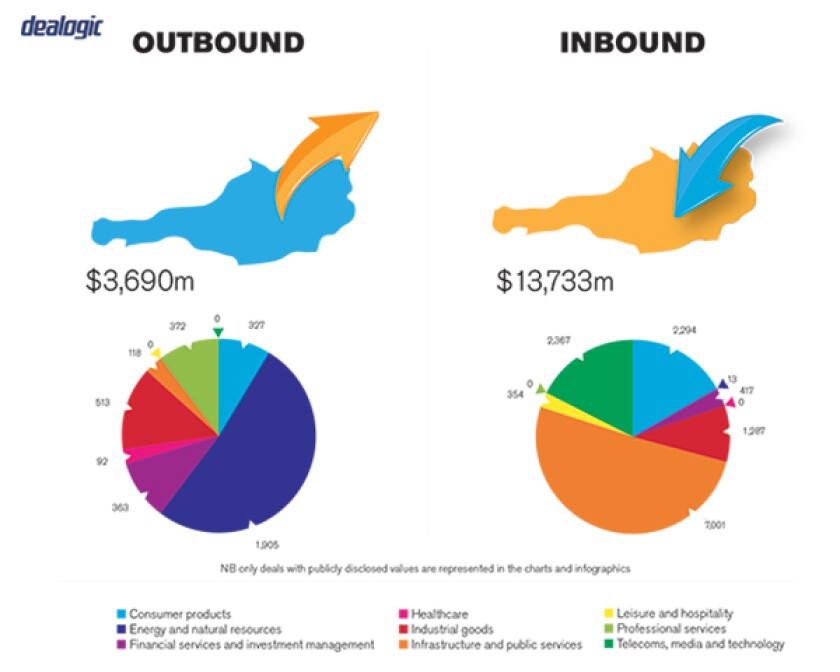

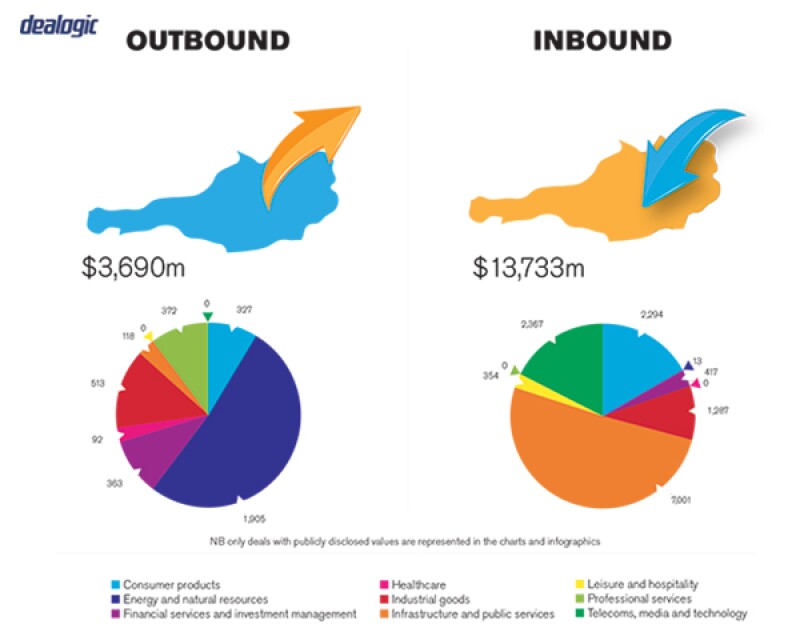

The majority of transactions was performed by means of a share deal, which is generally the typical means of acquisition of an Austrian company. An interesting aspect of M&A deals performed in Austria in 2017 was the continuing increase of foreign investments – outbound as well inbound – and a significant reduction of purely domestic transactions. This shows that the Austrian market is getting increasingly interesting for foreign investors in particular on the real estate sector where higher margins as opposed to traditional financial investments can be achieved.

2.2 What have been the most significant trends or factors impacting deal structures?

Most investments in the Austrian M&A market are strategic investments with an insignificant number of financial investors playing a role. It can be perceived that due to the low interest rates and high liquidity in the market investors are searching for projects with higher achievable margins, which can be found in the Austrian real estate sector. Due to the continuing digitalization, the technology sector has also become more and more interesting over the years.

SECTION 3: Legislation and policy changes

3.1 Describe the key legislation and regulatory bodies that govern M&A activity in your jurisdiction.

Austrian law does not have one specific law regulating all issues on the acquisitions of companies, but rather various different statutes apply, depending on the specific type and form of an acquisition.

For asset deals, in particular the regulations of Sec 1409 of the General Civil Code and Sec 38 of the Commercial Code are pertinent. Sec 1409 of the General Civil Code provides that a purchaser generally is jointly and severally liable with the seller towards the seller's creditors for any liabilities of the acquired business having their origin prior to the acquisition. The purchaser's liability is limited to the current net asset value of the acquired assets and applies in case the purchaser knew or should have known at the time of the purchase of the pre-existing liabilities. Sec 1409 of the General Civil Code is mandatory law and cannot be waived or amended by contract. Liability can be reduced if the purchase price payable by the buyer is used to pay off the debts of the business sold. Sec 38 of the Commercial Code provides that a legal entity, which acquires and continues a commercial business, is liable for all debts the former owner incurred in the course of business conduct, meaning even those which are not contractually agreed to be taken over by the buyer. Unlike liability under Sec 1409 of the General Civil Code, liability under the Commercial Code is not limited to the value of the acquired assets. Nevertheless, under Article 38 of the Commercial Code the seller and the buyer can agree to limit liability of the seller, such limitation of liability, however, being only valid if a timely notification to the commercial register is submitted or otherwise made public.

A key regulatory authority with regard to M&A transactions is the Federal Competition Authority (Bundeswettbewerbsbehörde), which is competent for the clearance of mergers if the transaction volume does not exceed the thresholds of the EC Merger Control Regulation, but exceeds the thresholds under Austrian competition law. Further relevant authorities are the Commercial Register Courts (Firmenbuchgerichte), which register and publish transactions and reorganizations in the Austrian commercial register, and the Financial Market Authority (Finanzmarktaufsicht), which reviews banking acquisitions. Public M&A transactions regarding listed joint stock corporations (Aktiengesellschaft) are also subject to the supervision of the Austrian Takeover Commission (Übernahmekommission), which monitors compliance with the Austrian takeover regulations and decides on all matters related to the Takeover Act.

Inbound Outbound |

|

NB: Values may exclude certain transactions, for example asset acquisitions/sales |

3.2 Have there been any recent changes to regulations or regulators that may impact M&A transactions or activity and what impact do you expect them to have?

A recent change, which has been made to the Austrian Cartel Act and which applies to all transactions closing after November 2017, extended the scope of transactions for which clearance by the Federal Competition Authority needs to be obtained.

Another major change that will affect public M&A transactions as of January 3 2018 is the introduction of the possibility of a de-listing in the Austrian Stock Exchange Act (BörseG), which was introduced in order to adopt new EU investor protection and capital markets transparency regulations. The requirements for such a de-listing process is the affirmative resolution of a qualified majority in the annual general meeting and the prior active official listing over a period of three years. Besides this regular de-listing, a so-called "cold de-listing" (meaning de-listing due to corporate law measures such as a merger) was also introduced. The motivation for such delisting could be rooted in economic factors, such as conflicts between the supply and demand sides or due to company internal initiatives to avoid the transparency rules and competitive disadvantages associated with the stock exchange regulation.

3.3 Are there any rules, legislation or policy frameworks under discussion that may impact M&A in your jurisdiction in the near future?

In October 2017, federal elections took place in Austria, which brought a change of political power. The new government was established in December 2017. It remains to be seen which changes with relevance to the Austrian M&A market the new government intends to implement. According to the government program, the new government intends to dissolve hurdles and simplify administrative proceedings, which might also have an effect to M&A in Austria.

SECTION 4: Market idiosyncrasies

4.1 Please describe any common mistakes or misconceptions that exist about the M&A market in your jurisdiction.

The Austrian legal system has a few peculiarities, which are commonly misunderstood. As most M&A deals in Austria are private M&A transactions, where the target company is an Austrian limited liability company, the share deal must be made in the form of a notarial deed in front of an Austrian notary public. Typically, such notarial deed needs to be drawn up in German. With the increasing foreign involvement in Austrian M&A transactions, it has become more and more common that such notarial deeds may also be drawn up in English.

Misconceptions also exist with regard to the fact that certain transactions in Austria are subject to Austrian stamp duty tax. Typically, stamp duty tax becomes payable upon the simple fact that a written document on a transaction is being drawn up in Austria. A lot of misunderstandings with regard to stamp duty tax can be resolved if professional advice is sought at an early stage.

4.2 Are there frequently asked questions or often overlooked areas from parties involved in an M&A transaction?

The concept of the Austrian stamp duty tax often requires specific legal advice in particular as to possibilities to legally avoid such stamp duty tax.

For real estate transactions, it is advisable to seek preliminary advice in order to properly structure the acquiring vehicle to minimize possible tax implications connected with the transaction.

4.3 What measures should be taken to best prepare for your market's idiosyncrasies?

In order to best prepare for Austrian particularities and idiosyncrasies, it is advisable for foreign investors to seek legal and tax advice by Austrian specialists at an early stage. That way the acquisition of a possible Austrian target company can be structured in the best possible way to meet the investor's needs and comply with Austrian particularities.

SECTION 5(a): Public M&A

5.1 What are the key factors involved in obtaining control of a public company in your jurisdiction?

Most determinants regarding the acquisition of a controlling stake in a public company are regulated in the Austrian Takeover Act. A compulsory public offer has to be made to the other shareholders when a shareholder acquires a stake of 30 % or more.

5.2 What conditions are usually attached to a public takeover offer?

Pursuant to Sec 5 para 2 of the Austrian Takeover Act, the intention to acquire a stake in a public company needs to be communicated as soon as there are rumours that could alter the stock price. The bidder who is intending to place an offer also has to inform the target's representatives immediately, notifying them that the executive board and the supervisory board have decided to place such offer, or that conditions have been met that oblige them to place an offer. Public takeover offers need to be executed in a way that minimise market manipulation and insider trading. The members of the target company also have corresponding secrecy and transparency duties. A further condition is the notification of the workers council pursuant to Sec 11 para 3 of the Austrian Takeover Act. A financial expert must also be included in the public takeover offer process.

5.3 What are the current trends/market standards for break fees in public M&A in your jurisdiction?

Break fees or break-up fees, as well as termination fees, have found their way into Austrian M&A practice especially since the financial crisis. These fees can amount up to 20 % of the transaction volume. In public M&A transactions, such fees are rather uncommon, which is partly due to legal restrictions, whereas in private M&A transactions, break fees are more often agreed upon.

SECTION 5(b): Private M&A

5.4 What are the current trends with regard to consideration mechanisms including the use of locked box mechanisms, completion accounts, earn-outs and escrow?

The purchase price in private M&A transactions is typically either fixed under a locked box mechanism or determined at signing as a provisional purchase price pursuant to a fixed calculation method which is then finalized on the basis of financial accounts drawn up at closing. Earn-out mechanisms are sometimes included as mechanisms to adapt the purchase price after closing. It is also quite common to place a certain percentage of the purchase price in escrow at signing, of which a designated amount might also be used as break fees in case the deal does not close.

5.5 What conditions are usually attached to a private takeover offer?

Typically, the private takeover offers are conditional upon a satisfying due diligence and transaction documentation, approvals of internal boards and committees, the conclusion of certain side agreements which are deemed necessary and the occurrence of no material adverse changes.

5.6 Is it common practice to provide for a foreign governing law and/or jurisdiction in private M&A share purchase agreements?

No, generally the parties of a private M&A share purchase agreement agree on Austrian substantive law and dispute resolution in Austria. This also relates to the fact that mandatory Austrian laws apply to the acquisition of shares in an Austrian company.

5.7 How common is warranty and indemnity insurance on private M&A transactions?

W&I insurance as a tool coming from the Anglo-American tradition is available but still not very common in the Austria M&A market. However, throughout Europe it is getting more and more common to make use of this useful tool. We believe that this trend will gradually also be implemented in the Austrian M&A market.

5.8 Discuss the exit environment in your jurisdiction, including the market for IPOs, trade sales and sales to financial sponsors.

IPOs do not play a significant role on the Austrian market. Generally, a shareholder interested in selling his shareholding will initiate a structured bidding process to which interested parties are invited. As the Austrian market is rather small, very often the shareholder will be aware of potentially interested parties and address them directly.

SECTION 6: Outlook 2018

6.1 What are your predictions for the next 12 months in the M&A market and how do you expect legal practice to respond?

The Austrian M&A market will continue to be influenced by macroeconomic developments (such as Brexit and general economic developments). Due to the persistent low interest rates and existing high liquidity in the market, investors will keep searching for projects with higher achievable margins. We believe that as in previous years, the focus will remain on the real estate and technology sectors. We also expect that the trends of previous years, relating to the continuing increase of transaction volume, will continue into 2018.

About the author |

||

|

|

Markus Fellner Partner, Fellner Wratzfeld & Partners Vienna, Austria T: +43 1 53770 311 F: +43 1 53770 70 W: www.fwp.at Markus Fellner is a founding partner and the head of the firm's corporate and M&A practice who specialises in banking and finance, insolvency law and restructuring and dispute resolution. He was admitted to the Austrian Bar in 1998 and lectures at various institutions, having been awarded a Mag IUR from the University of Vienna and a Mag RER SOC OEC from the Vienna University of Economics and Business. |

About the author |

||

|

|

Irena Gogl-Hassanin Partner, Fellner Wratzfeld & Partners Vienna, Austria T: +43 1 53770 372 F: +43 1 53770 70 W: www.fwp.at Irena Gogl-Hassanin is contract partner at fwp specialising in corporate and M&A, banking and finance, insolvency law and restructuring, company law and aviation law. She obtained her master of laws degree from University College London. Irena Gogl-Hassanin is author of several publications in her areas of specialisation and a part-time lecturer for finance at an Austrian university. |