MARKET OVERVIEW

Although the domestic Chinese M&A market continued to be active from January to November 2018 it appears that the overall number of cross-border M&A transactions decreased. This is possibly due to China tightening up its outbound investment and foreign investment control policies in respect of some typical Chinese outbound investment destinations, such as the US, UK, Germany and Australia. It is reported, however, that M&A transactions among 'Belt and Road countries' continue to grow.

M&A activity

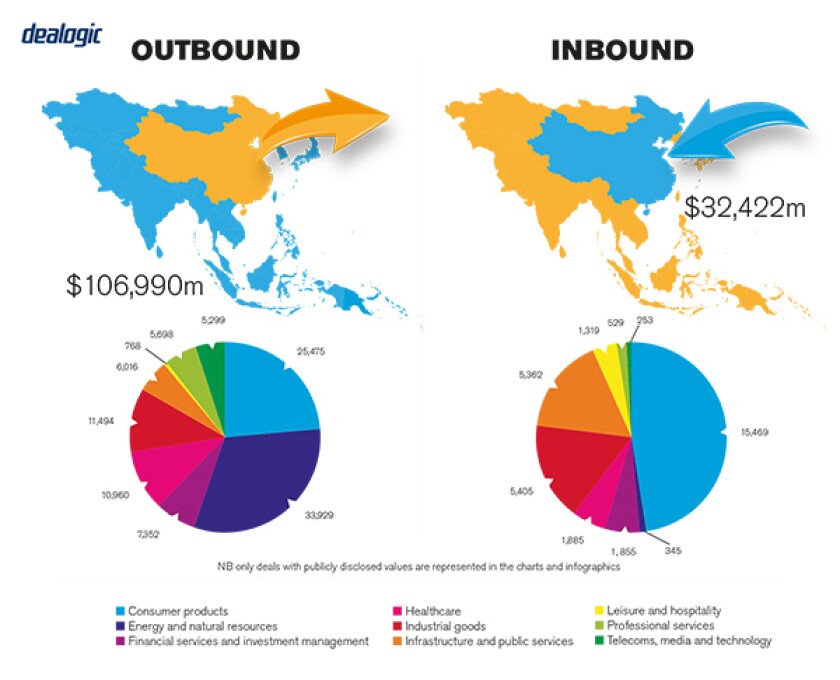

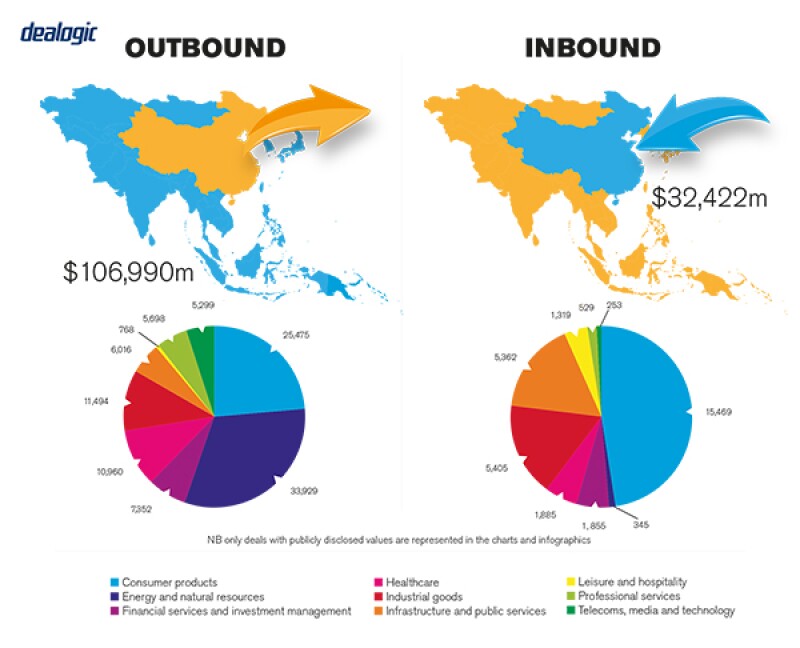

According to data from China Venture, total China M&A deal volume from January to November 2018 was 6,308 transactions. This represents a 14.69% decrease from the 7,394 deals recorded during the same period in 2017. The total deal value from January to November 2018 was $472 billion, which is 5.65% lower than the $501 billion in 2017. Inbound transactions roughly mirrored this decrease as the total number of inbound deals fell by a large margin, while the total deal value decreased but less significantly. The data for outbound deals suggested the opposite: the total number of outbound deals fell only a little, however the total deal value dropped significantly. As for specific industries, TMT and life science M&A remained active, while M&A in the manufacturing sector appeared to grow more quickly than others.

The Chinese M&A market is driven by both public and private M&A. According to data from China Venture, from January to November 2018, private equity (PE) and venture capital (VC) transactions accounted for the majority of the total deal volume, while public M&A transactions account for the majority of the total deal value of M&A transactions.

TRANSACTION STRUCTURES

Notable factors in transaction structures include industry and form of assets, market share of the target or acquirer (in the cases of strategic investors), founder background, and the regulatory and political environment. For example, direct outbound M&A transactions further decreased due to more stringent CFIUS rules and new FDI restrictions adopted by European countries. Simultaneously, many Chinese investors continue to use offshore transaction structures for both outbound and inbound deals.

Financial investors

Financial investors are a significant driver of M&A activity in China. They contribute materially to the selection and development of investment targets and tend to lead overall investment trends in specific industries. It is widely accepted that the highly competitive PE and VC markets in China contributed to China's record high valuations for start-up companies from January to November 2018.

Recent transactions

In April 2018, Alibaba Group Holding acquired all outstanding shares not already owned by Alibaba in ELE.me at an implied enterprise valuation of $9.5 billion, which was reportedly one of the highest-valued transactions in the TMT sector in China in 2018. Post-acquisition, ELE.me is expected to be a part of the 'new retail' cluster in the 'Alibaba business ecosystem' to create a brand-new local living service. Almost at the same time, Meituan Dianping, a Tencent-controlled company, acquired Mobike – the current market leader in the bike sharing space – for $2.7 billion. Similar to the ELE.me acquisition, Meituan Dianping appears to envision the addition of Mobike as furthering its goal of forming a "closed-loop shopping experience".

The above two deals show the continued dominance of the so-called BAT companies (Baidu, Alibaba, Tencent) in the local M&A market. These companies – along with JD.com – are significant drivers of M&A activity in China, both in terms of value and volume. A key component of their respective acquisition strategies is expected to be industrial chain integration, with an overall commitment to building closed online-to-offline commerce chains. Moreover, it shows that there is – and is expected to continue to be for years to come – significant activity and fierce competition in the new retail space and among BAT companies.

LEGISLATION AND POLICY CHANGES

The key legislation governing M&A activity in PRC includes:

the PRC Company Law, the PRC Contract Law and judicial interpretations of the Supreme People's Court on their application;

the current foreign investment regulations, including the Provisions for Guiding the Foreign Investment Direction, the Catalogue for the Guidance of Foreign Investment Industries (2017 Revision), the Special Administrative Measures for Access of Foreign Investment (Negative List) (2018 Edition), and Special Administrative Measures (Negative List) for Foreign Investment Access in Pilot Free Trade Zones (2018 Edition), together with their implementation rules;

Chinese outbound investment regulations;

PRC foreign exchange laws and regulations;

company registration laws and implementation rules;

the PRC Enterprise Income Tax Law and its implementation rules; and

anti-trust-related laws, including the Anti-Monopoly Law and Guiding Opinions of the State Administration for Market Regulation on the Declaration of Concentration of Business Operators (2018 Revision).

The key regulatory bodies governing M&A activity in the PRC include:

The State Administration for Market Regulation (SAMR)

The State Administration of Taxation (SAT)

With respect to outbound, inbound or cross-border M&A, the Ministry of Commerce (Mofcom), the National Development and Reform Commission (NDRC), and the State Administration of Foreign Exchange (SAFE)

With respect to public M&A, the China Securities Regulatory Commission (CSRC), the Shanghai Stock Exchange (SSE), and the Shenzhen Stock Exchange (SZSE)

With respect to anti-trust issues, the Anti-Trust Bureau of the SAMR (which recently replaced Mofcom in regulating anti-trust filings)

Specific industry regulators may also be relevant, such as the Ministry of Industry and Information Technology (telecoms and IT sectors), Ministry of Education, the National Medical Products Administration, and the National Radio and Television Administration.

Recent changes in law

Recently, Mofcom and the NDRC promulgated shortened versions of their negative lists for foreign investment in China and domestic Pilot Free Trade Zones, effective on July 28 2018 and July 30 2018, respectively. The new lists expanded access to foreign investment in certain sectors, including finance, transportation, energy, resource, auto and agriculture, etc. More specifically, the nationwide list removed restrictions on foreign shareholding in the banking industry, relaxed the foreign shareholding ratios in securities, fund management, futures and life insurance companies to up to 51%, and also removed restrictions on manufacturing of special purpose motor vehicles and new-energy vehicles. As a result, we expect there to be an uptick in M&A transactions and foreign investment generally in these areas in the near future.

Regulatory changes under discussion

On December 26 2018, the Standing Committee of the National People's Congress released the draft Foreign Investment Law of PRC (Draft Foreign Investment Law) for public comment. If enacted, it would serve as the unified and primary legislation governing foreign investments and would overhaul the current set of foreign investment laws and regulations in place in China.

The Draft Foreign Investment Law aims to promote equal treatment of foreign-invested enterprises (FIEs) and domestic enterprises in terms of the application of polices, industrial standards and government procurement, and to strengthen protection for foreign investments in China. For example, it expressly provides that profits, capital gains, royalties from IP licensing, and other lawfully obtained compensation or indemnification proceeds can be freely remitted out of the PRC.

However, in contrast to the previous draft Foreign Investment Law promulgated for public comment in 2015, the Draft Foreign Investment Law does not expressly address VIE structures, which are widely used by foreign investors in China's M&A market. As the Draft Foreign Investment Law is still very general at this time, we expect to see further implementation rules and guidelines following its enactment.

MARKET NORMS

Regarding market practice, a common error that some investors make is that they tend to neglect the importance of prudent due diligence and an informed decision-making process during the execution of M&A deals. Timetables can be unreasonably aggressive in a rush to close a deal and save on transaction costs. This may result in material issues in terms of compliance, internal control and contingent liabilities arising shortly after closing, causing unrecoverable losses for the investors. Potential investors are therefore advised to engage experienced lawyers, accountants, tax advisors and other professional advisors to conduct thorough due diligence on the target and to carefully assess relevant risks before making an investment decision.

Frequently overlooked areas

In domestic M&A deals, it is common for legal counsel to reuse transaction document templates from other jurisdictions. Often, those templates contain mechanisms tailored to the legal rules of another jurisdiction, or "tested language" that may have been vetted in US or UK courts, but remains untested in China. The enforceability of these provisions – even fundamental terms, such as those relating to signing formalities – should not be taken for granted. Potential investors should ensure the terms are carefully reviewed from a PRC law perspective to ensure maximum enforceability in PRC legal proceedings.

PUBLIC M&A

The Shanghai composite and main Shenzhen index dropped by more than 20% and 30%, respectively, in 2018. Many PRC public companies defaulted on debt and are generally facing financial difficulties. Therefore, PRC investors (especially the state-owned enterprises) have become more active in attempting to obtain control of public companies in 2018. However, not many deals were closed due to stock price fluctuations and disagreements on key deal terms.

Competitive or hostile takeovers are rare in the PRC market.

The key factors at play when obtaining control of a public company in China include: (i) deal structure: share transfer by agreement, voting trust, block trade, tender offer (or a combination of these); (ii) fluctuation of share price and liquidity of shares; (iii) lock-up periods; (iv) the source of funds and form of payment (by cash or share swap); (v) the buyer's own track record in terms of legal compliance, securities actions and leverage ratio; (vi) potential subsequent transactions, ie whether the buyer will inject assets into or merge with the public company after obtaining control, which may constitute a back-door listing, making it subject to CSRC approval; (v) other regulatory approvals for the transaction, for example, if the buyer is a foreign company, it is subject to Mofcom approval for acquiring shares of a PRC public company.

Conditions for a public takeover

Chinese investors prefer to obtain control of a public company by agreement rather than by a public takeover offer. This is partly because upon the announcement of a tender offer, the share price of the target company tends to go above the tender offer price, making the latter unattractive. But this changed somewhat in 2018 due to turbulence in the market: a few successful tender offer deals have been seen in the past year, and other deals, consummated through a combination of share transfer agreement and tender offer, were announced as well. The key players in such deals tend to adopt more creative and flexible deal structures to mitigate their downside risks as well.

Common conditions attached to a public takeover offer include: (i) compliance with the disclosure rules of the stock exchanges, (ii) the buyer's track record in terms of legal compliance, securities actions and debt status, which should meet the applicable legal requirements; (iii) submission of a takeover offer proposal to the stock exchange and the CSRC for approval; (iv) there being no objection raised by the CSRC or the relevant stock exchange; and (v) the source of funds and offer price meeting applicable requirements.

According to the Administrative Rules on Acquisitions of Listed Companies and relevant disclosure rules under PRC law, the purchase of a public company in an all cash deal is not subject to CSRC or stock exchange approval. However, in practice, the stock exchanges in China will issue an inquiry letter and substantively review the qualifications of the buyer, the legality of the deal terms and source of funds and other deal points. It is not uncommon that the purchase proposal would be 'rejected' by the stock exchange if it deems the buyer non-compliant with any legal requirements or to be lacking the funds for the acquisition.

Break fees

Due to the uncertainty of obtaining regulatory approval and high purchase prices, more and more companies are adopting break fee mechanisms in public M&A deals, including reverse break fees, often linked to approvals and financing conditions.

PRIVATE M&A

For PRC M&A deals, lock-box mechanisms and earn-outs are more commonly used by the parties than completion and escrow accounts. Due to relatively high valuations, buyers tend to favour earn-out mechanisms, based on multiples of EBITDA or net profits post-closing, to allow for valuation adjustments and market shifts. Strategic investors also often use earn-outs to motivate founders/management to focus on maximising growth in the years immediately following the transaction. Escrow arrangements are not frequently used in purely domestic PRC M&A transactions, due to local restrictions, although they are more common in cross-border deals in which all or a portion of the purchase price is paid at the offshore level. In addition, it is not currently common for parties to purchase representations and warranties insurance in PRC private M&A transactions.

Conditions for a private takeover

The conditions attached to a private takeover offer usually include: consideration amounts and mechanism, form (cash or equity/share), payment schedule; deal structure; key closing conditions and timeline, such as obtaining regulatory approvals/filings; tax obligation allocation; strategic cooperation terms (for strategic investors), and; break fees.

Foreign governing law

Where a purely domestic company is being purchased or invested in by a foreign buyer, it will be mandatory for the share purchase agreements (SPAs) to be governed by PRC law. For cross-border M&A deals, parties may be able to choose the laws of another jurisdiction to govern the key SPAs, subject to the Law of Application for Foreign-related Civil Relations. The selection of the laws of a given jurisdiction to govern a share/equity purchase agreement will be determined based on a number of factors, including the deal structure, the nationality of the purchasing entity, the qualification of their legal counsel, etc.

The exit environment

In China, it can take as long as three to five years for an IPO to be approved after initial filing. The number of IPOs declined by 74% in 2018 compared to 2017. Although there are fast-track exceptions, such as Foxconn (which took only 40 days to complete its IPO), most applicants would still have to wait in the lengthy multi-year queue and be subject to CSRC scrutiny before getting listed. As a result, many PRC-based companies (especially fast-growing high-tech companies) are drawn to the US and Hong Kong IPO markets, and adopt offshore structures and VIE arrangements accordingly.

Another way to exit in the Chinese market is via a share swap with a public company. As this may or may not constitute a back-door listing in China, this type of deal structure tends to be subject to strict scrutiny by the CSRC. The market has seen a large number of applications rejected in 2018, especially in the media and entertainment industry.

As a result, many investors resort to trade sales as a common exit alternative, for example a strategic sale to a BAT company. Those sales tend to be more market oriented, depending on the targets' market share, financial performance, growth prospects, etc.

OUTLOOK

Market activity in 2019 is expected to slow further. However, we are cautiously optimistic that the optimisation of M&A policy and other policy reforms – some of which may correlate with the thawing of trade tensions between the US and China – could help to spur market activity. In many markets and industries, further integration will likely be inevitable, but could be delayed (though probably not stagnated) by macroeconomic conditions. In the near future, as the PE/VC market cools and valuations drop (and as financial investors begin seeking exit opportunities), we believe there will be an uptick in M&A activity by strategic investors in the PRC both in 2019 and the years following.

About the author |

||

|

|

Julia Dai Partner, DaHui Lawyers Shanghai, China T: +86 21 5203 0688 F: +86 21 5203 0699 Julia Dai is a partner in DaHui Lawyers' corporate/M&A practice group. Her practice focuses on corporate and finance transactions, including capital markets, M&A and strategic investments. Julia has extensive experience in complex cross-border M&A, along with private equity & VC investments both in China and overseas. |

About the author |

||

|

|

Jenny Li Partner, DaHui Lawyers Beijing, China T: +86 10 6535 5888 F: +86 10 6535 5899 Jenny Li is a partner in DaHui Lawyers' corporate/M&A practice group. Jenny's industry experience is primarily focused in the internet, film, entertainment, technology and media sectors, as well as in the traditional manufacturing sectors. She has a wealth of diverse experience in listings in domestic and foreign markets, follow-on offerings, major asset restructurings for public companies and M&A deals. |