The environment in Switzerland continues to be very favourable for both public and private M&A transactions and this was reflected in the high M&A activity in 2019. The reasons for the high activity in the M&A market are manifold. The absence (or near absence) of investment restrictions in Switzerland facilitate investments. Various sectors (for example healthcare and IT) are facing a consolidation wave, which further increases M&A activity. Many Swiss companies, especially small- and medium-sized enterprises (SMEs), are working through succession planning in the coming years and are therefore attractive investment opportunities. Swiss companies continue to transform and reshape their portfolios through M&A transactions. This environment characterised (still) by low interest rates and generous borrowing conditions continues to facilitate funding of possible acquisitions and puts pressure on investors to invest. Finally, M&A remains an important opportunity for growth.

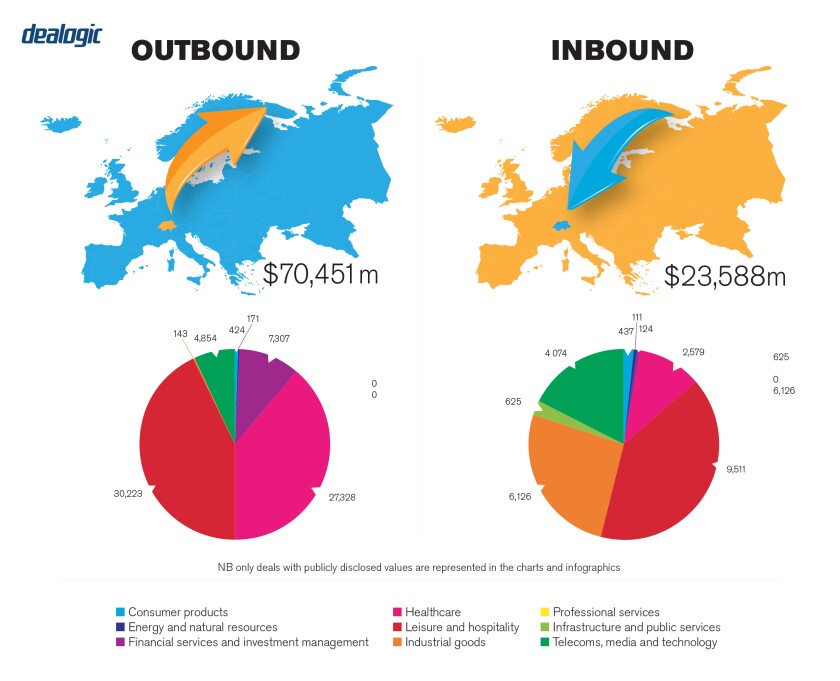

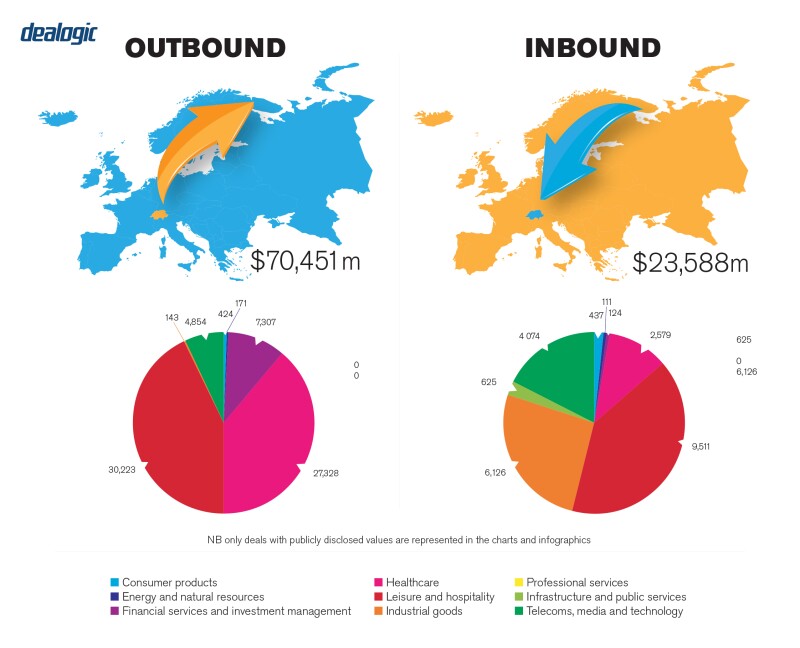

After all-time record deal volumes in 2018, activity in Switzerland only declined slightly in 2019. M&A deal flow and volume was particularly high in the chemicals, technology, media and telecoms as well as in the pharmaceuticals and life sciences sectors, which even saw increases in transaction figures (overall both in terms of deal numbers and deal values).

Private equity investors were involved in almost half of the 50 largest deals involving Switzerland in 2019.

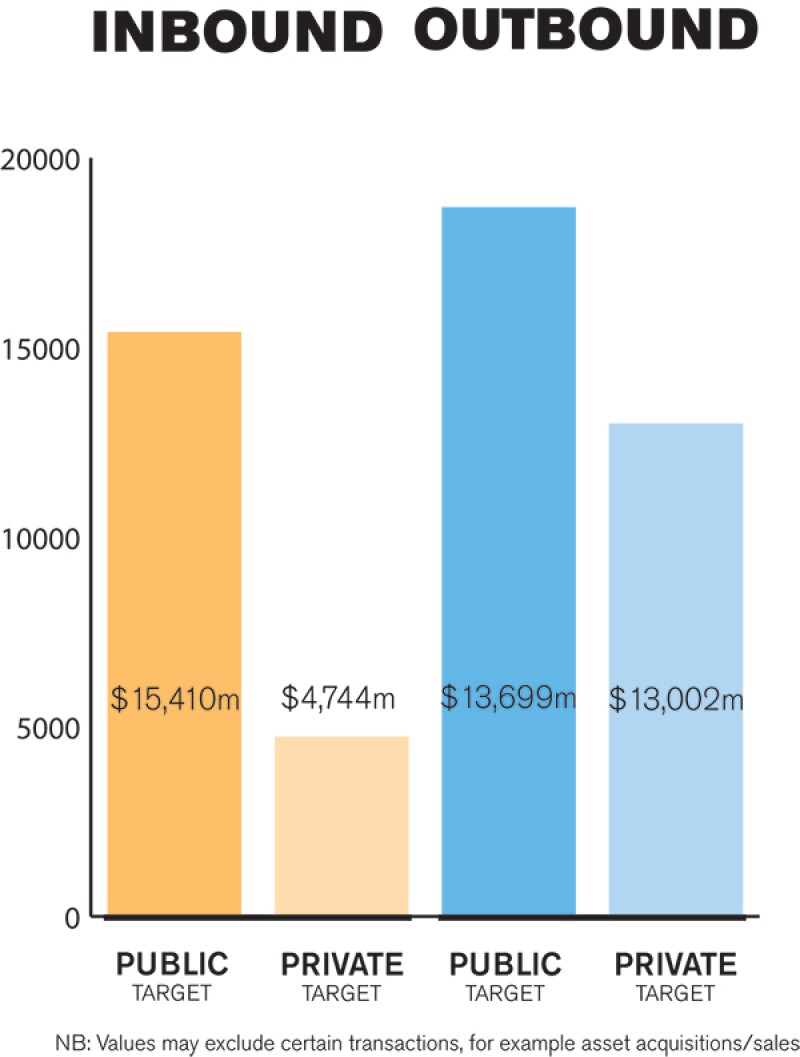

Private M&A transactions accounted for most of the overall Swiss M&A market both in terms of number of deals and deal value in 2019. However, private M&A activity is often fuelled by public M&A and vice versa. For example, taking-private a company by way of a public tender offer and subsequent squeeze out is often followed by subsequent disposals or bolt-on acquisitions to focus, transform or grow the business. For private equity in particular, IPOs have gained in importance in exit strategy considerations either as a standalone solution or as part of a dual-track process (more on this below).

TRANSACTION STRUCTURES

We see the following three trends influencing deal structures (and generally leading to M&A activity): industry consolidation, focused on the healthcare sector; transformation and portfolio reshaping; and M&A as a growth opportunity.

Private equity firms were very active in Switzerland in 2019, with 126 deals (-21% compared to 2018). Even though the number of deals fell slightly compared to 2018, larger transactions helped to keep total deal value at the 2018 level. In order to cope with rising valuations, private equity firms are increasingly pushing to break new grounds – straight forward deals have become rare. For example, one strategy of private equity firms is to acquire different companies in the same or similar industries and to try to realise synergies. Further, private equity firms tend to do larger deals (for example, the acquisition of Nestlé Skin Health by EQT). The M&A environment in Switzerland has consequently become more competitive, more sophisticated and bolder. While the number of campaigns by activist shareholders in Switzerland is still relatively low compared to the US for example, activist shareholders also played an important role in 2019. ABB's CEO, Ulrich Spiesshofer, stepped down in 2019 after almost six years and following years of pressure from investors (in particular from activist shareholder Cevian Capital, which supposedly pushed the sale of ABB's power-grid division to Hitachi).

2019's largest transaction in Switzerland involving a private equity firm was the acquisition of Nestlé Skin Health by a consortium led by EQT and the Abu Dhabi Investment Authority (ADIA). With a transaction volume of more than CHF10 billion ($10 billion) this deal proves private equity's ability to structure and execute transformational transactions on a global scale.

Another (purely Swiss) deal that is noteworthy was the sale of Swiss broadcasting group 3 Plus Group to CH Media, one of the largest media companies in Switzerland. The transaction is further proof of the high activity in the TMT sector and the consolidation wave.

One of the most controversially discussed deals of 2019 was the failed acquisition by Sunrise Communications of UPC Switzerland. Amid opposition by Sunrise's largest shareholder Freenet and other investors, as well as proxy advisors, Sunrise cancelled the extraordinary general meeting which was to approve the required CHF2.8 billion capital increase. The costs incurred by Sunrise and the CHF50 million break fee triggered by the termination of the agreement with UPC owner Liberty Global came under increased scrutiny following the cancellation.

LEGISLATION AND POLICY CHANGES

Public tender offers for companies whose equity securities are (fully or partially) listed on a Swiss exchange (in case of non-Swiss domiciled issuers only if the main listing is in Switzerland) are subject to Swiss public takeover law. The central piece of legislation regulating public tender offers is the Financial Market Infrastructure Act (FMIA) and its implementing ordinances, particularly the Takeover Ordinance (TOO). The primary goal of the legislation is to ensure equal treatment of a target's shareholders. The Swiss Takeover Board (TOB) is tasked with ensuring compliance with takeover law. It is supervised by the Swiss Financial Market Supervisory Authority FINMA which, among other, is the appeal body for parties challenging TOB decisions.

Private M&A transactions are a lot less regulated and parties have far-reaching freedom in determining the contractual rules that should apply. Depending on the involved parties and the nature of the transaction other legislation may need to be observed, such as the Antitrust Act and the Act on the Acquisition of Real Estate by Persons Abroad (so-called Lex Koller).

The Financial Services Act (FinSA), the Financial Institutions Act and their respective implementing ordinances entered into force on January 1 2020 (with some provisions being subject to transition periods). The FinSA contains rules regarding the duty to publish a prospectus in the case of a public offering of securities, including minimum content requirements, and brings these requirements in line with international standards and the standards that had already been applied by SIX Swiss Exchange for listing prospectuses. It also provides for certain specific exemptions from the duty to issue a prospectus. The provisions of FinSA will typically become relevant in the context of M&A if, in a public tender offer, securities are offered as consideration to the target's shareholders. While the FinSA provides for an exemption from the prospectus requirement in a public takeover, the exemption is subject to equivalent information being available. An offeror in a public takeover would therefore need to satisfy both the requirements under FinSA and the less stringent requirements of Swiss takeover law.

Further, the regime for the disclosure of the beneficial owner of shareholders acquiring, alone or in concert with third parties, more than 25% of the shares in a company was amended with effect from November 1 2019. The amendments removed some of the uncertainty of the old rules. They also clarified that where there is no beneficial owner (i.e., no natural person exercising direct or indirect control over the acquiring shareholder) the shareholder must make a negative declaration.

Even though some politicians promote and favour investment restrictions for critical infrastructure in Switzerland (for example in power supply, oil supply, natural gas supply and district and process heat etc.), no such restrictions are currently in force nor being planned by the Swiss legislator.

MARKET NORMS

A common misconception about the Swiss M&A market is that Switzerland only offers targets in the financial industry. In 2019, M&A volumes in the financial industry fell to an all-time low and only accounted for 7% of transactions.

It is also noteworthy that other than transactions involving regulated financial institutions and transactions subject to antitrust approval, most M&A transactions require no approval or consent in Switzerland by regulatory or governmental authorities

In almost every case, the chain in the ownership of Swiss target companies cannot be fully traced back to incorporation. Sellers planning a transaction should therefore initiate the title clean-up well before starting the sales process in order not to jeopardise the timeline.

In Switzerland, the use of artificial intelligence, machine learning (for example, Luminance or Kira) and big data continues to increase. Digitalisation is becoming increasingly important for Swiss law firms on their journey to increase efficiency.

PUBLIC M&A

In an ideal scenario an offeror holds more than 98% of the voting rights in the target company following a public tender offer as this allows the offeror to file for cancellation of the remaining shares in a statutory squeeze-out court procedure pursuant to the FMIA, against the payment of the offer price to the holders of the cancelled shares. If the offeror falls short of the 98% threshold but holds at least 90% of the voting rights, full ownership can be achieved through a squeeze-out merger pursuant to the Swiss Merger Act which, however, carries a higher litigation risk than the FMIA procedure.

Therefore, an offeror will typically want to reach at least the 90% threshold in order to be able to obtain full control. In mandatory takeover offers, minimum acceptance threshold conditions are not permissible (more on this below). A voluntary offer, however, may be conditional on a minimum acceptance threshold, though only if the threshold is not unrealistically high, which the TOB assesses based on the circumstances of the specific case. Absent significant holdings by the offeror in the target company prior to the offer the TOB will typically not permit a condition requiring that the offeror reaches the 90% threshold.

|

|

MAC clauses have largely disappeared |

|

|

Swiss law allows hostile and friendly takeover bids, but an offer that is supported by the target company's board is more likely to be successful. In a friendly takeover, the offeror and the target company will normally enter into a transaction agreement pursuant to which the target's board of directors agrees to recommend the offer to its shareholders and not to solicit offers from third parties (but with a 'fiduciary out' in case of unsolicited superior offers).

The permissibility of conditions that may be attached to a public takeover offer depends on whether the offer is voluntary or mandatory. The duty to make a mandatory offer is triggered if the offeror acquires shares in a company exceeding the threshold of 33.33% of the voting rights or a higher threshold of up to 49% that applies pursuant to a so-called 'opting-up' clause in the target's articles of association (Swiss law also allows companies to opt out completely from the mandatory bid regime).

With respect to mandatory offers there is only a very limited number of offer conditions that the TOB deems permissible. These include that no injunction or court order prohibiting the transaction will be issued and that necessary regulatory approvals will be granted, as well as conditions ensuring the ability of the offeror to exercise the voting rights (i.e., entry in the share register and abolishment of any transfer and/or voting restrictions). In voluntary offers, the scope of admissible conditions is much wider, including minimum acceptance thresholds (see above) and no MAC conditions.

Break fees are generally considered permissible if the amount is set so as to compensate the offeror for the costs of a breakup. Break fees that have a punitive character and significantly restrict shareholders in their freedom to accept or not accept an offer and/or deter potential competing offerors may be invalid, although the question has not been answered conclusively in Swiss legal doctrine and case law to date.

PRIVATE M&A

Unlike in the US and Asia, locked-box pricing mechanisms are widely used and accepted in Switzerland. In particular in the current seller friendly market, sellers seeking to limit balance sheet risks and reduce the risk of post-closing purchase price adjustment disputes push towards using locked-box pricing mechanisms.

As a consequence of the current seller's market, locked-box pricing mechanisms are often combined with an interest payment or cash-flow participation for the period between the locked-box date and actual payment of the purchase price (closing), and buyers tend to accept longer periods between the locked-box accounts date and closing.

In the current seller's market, sellers usually push towards reducing conditionality to an absolute minimum in order to increase transaction certainty. In particular, MAC clauses have largely disappeared, but even the outcome of the merger control assessment may be a criterion for certain sellers to move forward with a specific bidder in an auction process. Further, we increasingly often see 'hell or high water' clauses included in the merger clearance closing condition.

In case of a Swiss target company, it is absolute market practice to agree on a Swiss law governed share purchase agreement with jurisdiction in Switzerland. In addition to the fact that this is generally expected by Swiss sellers (due to the well-known advantages of the application of domestic law and a domestic forum), various legal questions, such as the process of validly effecting the transfer of shares, the board representation, shareholder requirements etc., are not open to any choice of law but governed by Swiss law anyway.

Over the past years W&I insurance has increasingly been used in M&A deals in Switzerland. In this sellers' market we mainly see buyer polices which can be a solution to bridge the 'liability gap', where a seller is prepared to give representations and warranties but wants to cap its liability at a level that the buyer is not comfortable with and the W&I insurance can increase the overall cover available for the buyer.

In case the liability cannot be capped or excluded due to the lack of negotiation power of seller, seller policies are used (especially by financial sponsors) to shift the risk of potential outstanding claims to an insurer in order to be able to distribute the exit proceeds to the greatest extent possible to investors immediately following closing.

In cases where a private equity or other investor is invested in a target jointly with another party, the conditions under which the investor is able to exit as well as the exit route usually depend on the terms of the shareholders' agreement. The most prominent exit routes are (still) trade ales (either to a strategic investor or private equity firm), including secondary buyouts. Exits through an IPO on the SIX Swiss Exchange are still less common but have become more attractive in recent years. We are also observing a trend towards dual-track processes to increase deal certainty, specifically in times of volatile and unpredictable markets, and maximise valuation, despite the inherent complexity in running simultaneous IPO and M&A processes.

LOOKING AHEAD

Despite some uncertainties, such as global trade disputes, potential (minor) increases of interest rates or high valuations, we are positive that the Swiss M&A market will continue to be strong in 2020. Especially due to last year's healthy fundraising environment, we expect private equity firms to remain active on the M&A market. Lastly, since private valuations are generally at pre-crisis levels, public markets are becoming more attractive as they lose their liquidity premium. We therefore also expect that the pursuit of dual-track processes will continue in 2020.

About the author |

||

|

|

Daniel Raun Partner, Bär & Karrer Zurich, Switzerland T: +41 58 261 52 32 Daniel Raun advises listed and privately held companies on a broad range of corporate and commercial law matters. The focus of his work is on international and domestic M&A as well as capital market transactions. Daniel further specialises in corporate and regulatory matters affecting listed companies, with a focus on disclosure and reporting requirements under securities law and stock exchange regulations. |

About the author |

||

|

|

Philippe Seiler Partner, Bär & Karrer Zurich, Switzerland T: +41 58 261 56 48 E: philippe.seiler@baerkarrer.ch Philippe Seiler has broad experience in international and domestic M&A transactions in various industries. Philippe does not only cover big ticket transactions but also focuses on small- and mid-size M&A transactions, private equity transactions and venture capital and start-up transactions. Furthermore, he specialises in regulatory matters in the fields of life sciences and healthcare. |

About the author |

||

|

|

Raphael Annasohn Partner, Bär & Karrer Zurich, Switzerland T: +41 58 261 52 65 E: raphael.annasohn@baerkarrer.ch Raphael Annasohn has broad experience in international and domestic M&A transactions, corporate reorganisations and restructurings as well as corporate law and general contractual matters (in particular shareholders' agreements and employee participation plans). Furthermore, Raphael specialises in the fields of venture capital and start-ups and is the co-founder of Bär & Karrer's start-up desk. |