It is expected that all projects in Angola that were suspended in 2020 due to COVID-19, will be resumed in 2021. One of the main drivers will be the ambitious programme of privatisation, which includes privatising a total of 195 companies by 2022. Such a programme has never been seen before in Angola and includes companies in the oil and gas, diamonds, aviation and insurance sectors, among others. The most important companies in Angola are all expected to be privatised.

The M&A market is essentially controlled by private entities. However due to the privatisation plan, it is expected that the public entity intervention in the market will increase, particularly from the seller side.

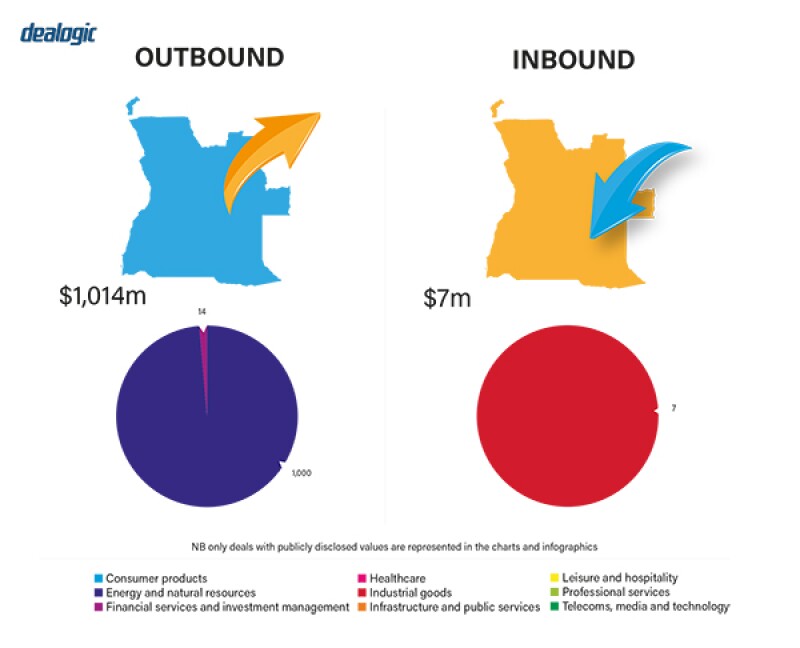

One of the main debates generated by M&A in Angola is related to the payment and transfer of dividends outside of the country. There are a lot of restrictions in place and this may impact M&A deals going forward, especially if some foreign shareholders are involved in the transaction.

COVID-19 and recovery plans

The COVID-19 pandemic has had a severe impact on Angola's economy. The government is adopting the necessary measures to deal with the situation and to reduce the impact of COVID-19, both in the labour market and other sectors of the economy.

The decline in oil prices has put further pressure on the economy, which depends heavily on oil exports. Angola is making a strong effort to stabilise the economy, control inflation, maintain the dynamism of reforms and safeguard financial stability. In terms of M&A and compared with previous years, there was a significant reduction in M&A operations. In 2021, one of the key areas for the market in Angola will be the privatisation of some public entities and concession of public services/infrastructure.

|

|

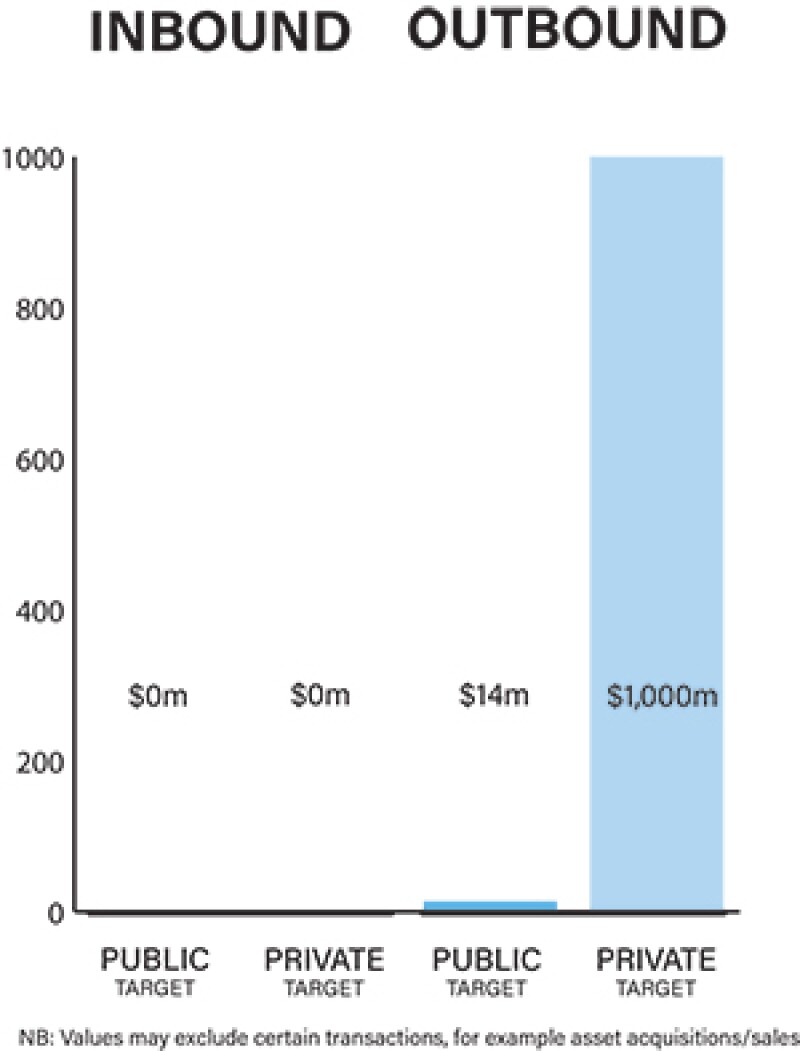

For 2021, the market is forecasting a substantial increase in M&A transactions |

|

|

The structure of transactions is mainly influenced by the fact that there is still a predominance of state-owned companies, a fact which increases transaction risk. There are other factors such as licensing procedures, the intervention of regulatory bodies and tax and environmental issues that also influence the deal structures.

There are still economic sectors dominated by state-owned companies. Privatisation will allow for a process of consolidation and a minimisation of the risks associated to private investment.

The most notable M&A transactions in the market have raised important issues and challenges, especially in competition law. As a factor for increasing credibility of the Angolan economy, the government has approved the legal regime for the protection of competition. This regime is applicable to all sectors of economic activity.

The debate on the implementation of this legal regime will most certainly affect the way M&A transactions are structured in Angola. There will be more control by the Angolan National Competition Authority over M&A activity. It is important to highlight that the new legal regime is very similar to the ones in force in several European jurisdictions; therefore, investors should be familiar with the new procedures and the new requirements.

The influence of financial investors has been significant because it has created more financing for transactions and boosted transaction volumes.

There has been a progressive increase of projects financed by international investment funds, some from Africa but also Europe, America and the Middle East. These funds present an interesting alternative to traditional financing.

The recovery of the M&A market will be highly dependent on the recovery of the world economy, especially of the countries of origin of fforeign direct investment (FDI). Nevertheless, the privatisation programme will contribute to a large extent to the sector's recovery.

Legislation and policy changes

The most relevant pieces of legislation for M&A in Angola are the following:

Law 1/04 of February 13 that approves the Companies Code and includes the rules applicable to each type of company;

Decree Law 42644 of November 14 1959 – Commercial Registry Code;

Law 10/18 of June 26 that approves the private investment legal regime and foresees the rights, undertakings and guarantees of the investors and the benefits and incentives attributable to investors;

Law 22/15 of August 31 that approves the Securities Code;

Law 5/18 of May 10 that foresees the competition legal regime applicable to all economy sectors;

Presidential Decree 240/18 of October 12 that regulates the competition law;

Law 5/97 of June 27 on exchange operations;

Law 11/2019 of May 14 2019 related to public–private partnerships;

Regulation 316/19 of October 28 2019 related to public–private partnerships;

Law 10/19 of May 14 that foresees the legal regime for the privatisation of state-owned companies; and

Presidential Decree 250/19 of August 5 2019 related to privatisation programme.

These are the main legal acts, although there are other applicable ones depending of the company's activity sector.

Regarding the public entities responsible for M&A processes, the investor will need to contact the Angolan Investment and Export Promotion Agency (AIPEX), the notary, the companies register, the competition authority and other regulatory authorities, depending on the business the targeted company operates.

|

|

One of the main debates generated by M&A in Angola is related to the payment and transfer of dividends outside of the country |

|

|

The main change in the legal framework regards the enactment of the competition law. After having identified some restrictive practices, the government decided to tackle the situation by adopting a new sanctions framework and new prior notification obligations, as well as by creating a requirement to obtain necessary permits from the competition authority in certain cases of company mergers. Not all transactions are subject to the competition law regime; only proposed mergers or acquisitions that exceed a certain turnover or market share threshold are subject to this regime and will need to seek approval of the competition authority.

The new private investment law should also be mentioned because it has established a set of principles and rules aimed at facilitating, promoting and accelerating investment operations in Angola.

Considering the high number of privatisations expected in 2021 and subsequent years, the decrees that will approve each privatisation and determine the conditions of each one is eagerly expected.

Market norms

There are sometimes misunderstandings on the part of international players due to the differences between the civil law system (Roman–Germanic family), to which the Angolan legal system belongs, and the practices of common law, typical in Anglo–Saxon countries which is what many of the investors into Angola's M&A market are familiar with. Many of the rules and practices applicable to M&A and to which UK and US companies are used to are not recognised or used in Angola.

Another difficulty lies in capital repatriation and currency fluctuations. These are most often considered as a limitation to bear in mind when analysing an investment process in Angola, especially when it is concluded by means of M&A.

Parties to a transaction seek legal advice at the first stages of a transaction; therefore, legal support extends from the early phases of negotiation, through the negotiation phase and until deal completion. This means that lawyers and other consultants intervene in the negotiation and drafting of memorandums of understanding (MoUs), non-disclosure agreements (NDAs), letters of intent, different types of agreements and in the due diligence process.

Technology may play an important role in Angolan M&A to speed up the efficient identification of prospective operations, in the negotiation of competitive offers and in reducing the times for analysing documents available in data rooms. Technology may also facilitate knowledge and aid evaluation and assimilation. The use of digital data rooms is very common and facilitates due diligence.

Public M&A

According to Angolan law, some M&A transactions are subject to approval by authorities. These include the regulated investment activities such as in banking and finance, oil, gas and mining.

Furthermore, labour unions also play an important role in M&A transactions because the law stipulates that they must be consulted whenever a transaction may lead to any change from the employees' perspective.

Public takeover offers are subject to the legal regime foreseen in the Securities Code (Law No. 22/15 of August 31 that determines the equal treatment of the offer targets with some exceptions foreseen by the law). This legal regime imposes the prior registration for the Offer with the Organismo de Supervisão do Mercado de Valores Imobiliários (Securities Market Supervision Entity). The registration request requires that several documents are filed.

Private M&A

Parties to a private M&A transaction in Angola have full autonomy in regard to consideration mechanisms. It is very common to find parties use locked-box mechanisms, as frequently handled in the Anglo Saxon and European practices.

Price and payment terms are issues usually subject to thorough negotiation between the parties. It is not uncommon to find M&A deals in which there are fixed price mechanisms, variable price mechanisms and even a combination of both. The financial system also makes available several tools, such as escrow accounts and bank deposits and guaranties to facilitate the completion of deals.

Private offers do not have to obey to pre-established rules or to a standard structure. Therefore, parties are free to negotiate conditions, with the following exceptions:

Private offers made by listed companies that have the obligation of reporting those operations to the Organismo de supervisão do Mercado de Valores Mobiliários for statistical purposes; and

The private offers in which there is no need for the distribution of a prospectus must mandatorily be notified to the Organismo de supervisão do Mercado de Valores Mobiliários.

Apart from these restrictions foreseen in the Securities Code, other restrictions may arise from the Articles of Association of the targeted companies – for example these can foresee the existence of different types of shares with different voting rights.

Although Angolan law follows the civil law system, it is common to see parties seek to use common law regimes particularly those of the UK and US. It is also common to have jurisdiction clauses choosing arbitration procedures governed by the laws of other countries or also by the UNCITRAL regulations.

Sales are usually made to strategic purchasers and/or commercial partners. This is the most common exit strategy in Angola.

Looking ahead

Due to the COVID-19 pandemic, Angolan M&A activity in 2020 was reduced overall. For 2021, the market is forecasting a substantial increase in M&A transactions, especially due to the privatisation programme, which aims to privatise 195 companies by 2022.

This programme represents a move towards a market opening and liberalisation of the Angolan economy, which would represent new ground for the country. It could lead to important transactions requiring an increasing recourse to lawyers and other consultants' services. The sectors included in the programme include banking and insurance, real estate, gas, air or sea transportation services, agriculture, diamonds, oil, and hospitality.

Click here to read all chapters from the IFLR M&A Report 2021

Nelson Raposo Bernardo

Managing partner

Raposo Bernardo & Associados

T: + 351 21 3121330

E: nrbernardo@raposobernardo.com

Nelson Raposo Bernardo is the managing partner of Raposo Bernardo & Associados. He is the head of the firm's banking and projects practices and co-heads the corporate practice. He has more than 25 years of experience as a lawyer in high-profile and complex legal operations.

Nelson is strongly experienced and reputed in legislating, being a co-author of the present Portuguese Securities Code and has led several legislative reform committees, in several countries, in banking, financial, insurance, projects, start-ups and venture capital areas. He regularly advises clients on transactional work in the banking, infrastructure and pharmaceutical sectors. His recent transactions include advising an international bank consortium on an aircraft portfolio financing, a Portuguese bank in relation to asset and portfolio structuring for securitisation purposes in the automotive industry, and working for a Japanese bank concerning international credit operations.

Nelson is a graduate of law from the University of Lisbon, and also earned a master's degree in juridical sciences (corporate law) from the same school. He is an assistant professor of corporate and commercial law at the University of Lisbon for almost 20 years and on a regularly basis teaches entrepreneurship, start-up, and management courses at INDEG-ISCTE Executive Education in Portugal.

Ana Cláudia Rangel

Senior associate

Raposo Bernardo & Associados

T: + 351 21 3121330

E: acrangel@raposobernardo.com

Ana Cláudia Rangel is a senior associate at Raposo Bernardo & Associados. She heads the labour law department and the Angolan practice, having dual Portuguese and Angolan nationality.

Cláudia has an extensive track record in the main economic sectors and has successfully advised many clients in their day-to-day activity and in company restructuring operations. She has over two decades of experience conducting many high-profile and complex operations on banking, civil, labour, insolvency proceedings and arbitration matters. She has represented major players in the banking, energy, real estate, tourism and pharmaceuticals sectors. Her recent transactions include advising a major Chinese bank on a facility loan agreement for an international credit transaction, a Japanese bank on operations of capital equipment finance involving finance leases, and a banking consortium of five banks to finance a large infrastructure project of over hundreds of million dollars.

Cláudia is a graduate of a law degree from the University of Lisbon. She writes regularly for legal and business journals and magazines, and is frequently invited to be a speaker in conferences and congresses to speak about her specialty areas.