Luky Walalangi, Miriam Andreta and Renansyah Jenie, Walalangi & Partners (in association with Nishimura & Asahi

MARKET OVERVIEW

The market in 2018-19 seems to be tuned more to private than public M&A. In terms of the national legal framework for businesses, there has been an effort by the government to create a more transparent environment through the introduction and implementation of the Online Single Submission (OSS) system, which allows for different kinds of business licences to be obtained and integrated electronically. In the past, this was done manually through various government institutions, a process that consumed more time, effort and cost for applicants.

M&A activity

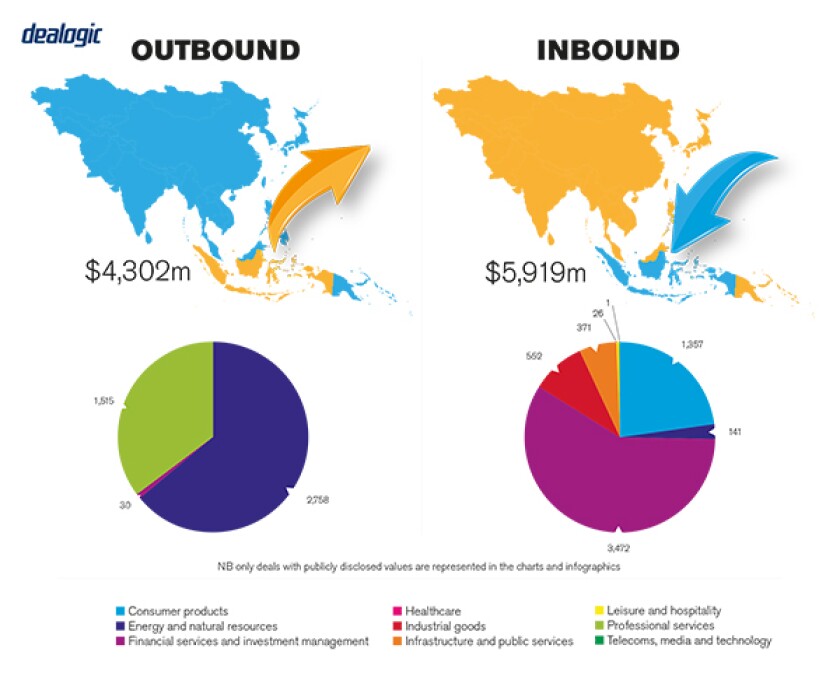

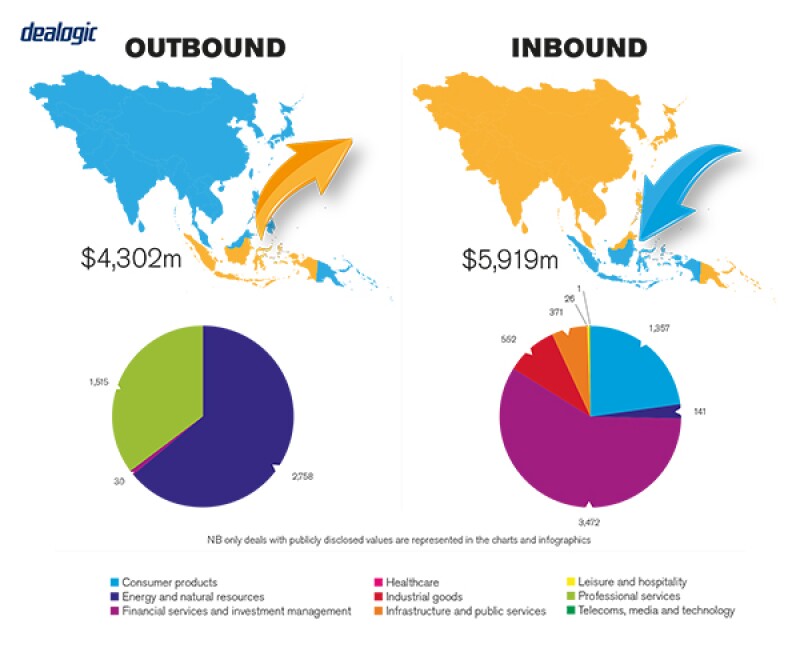

The Indonesian Business Competition Supervisory Commission (KPPU)'s website registered 69 M&A deals in 2018 that met the threshold for merger notification to the KPPU, with a total value of approximately IDR150 trillion ($10 billion). In addition, based on figures from the Indonesia Investment Coordinating Board (BKPM), investments from January 2018 to September 2018 reached IDR535.4 trillion.

Private M&A transactions still dominate the market (as confirmed by public data from the KPPU). The most sensible reasons are that the complex regulatory framework and procedures for M&A involving public companies often lead to lengthier deal times and costlier transactions.

TRANSACTION STRUCTURES

A sudden change in government policy and/or regulation is the most crucial influence on M&A deals, as these have a direct impact on financing strategies and how a deal is structured.

Financial investors

There has been some significant influence from financial investors acting as acquirers in Indonesian M&A transactions. Deals involving financial investors tend to have a quicker decision-making process compared to those involving traditional companies and the short-term investment/portfolio investment nature of financial investors has made Indonesian M&A more dynamic.

Recent transactions

One notable M&A transaction in the Indonesian market was the acquisition by Hokkan Holdings Corporation (Hokkan), one of the largest Japanese bottling and packaging companies, of the beverage package manufacturing business from seven companies belonging to PT Deltapack Industri (DPI Group) for IDR1.26 trillion. The transaction included the transfer and assignment of a substantial portion of DPI Group's moveable and immovable assets as well as business portfolios, which involved complex structuring and sophisticated multi-layered transfers of assets.

Other notable M&A transactions in 2018 included the acquisition of PT Freeport Indonesia by PT Indonesia Asahan Alumunium for IDR54 trillion and the acquisition of PT Bank Danamon Tbk. (Danamon) by Bank of Tokyo-Mitsubishi UFJ Financial Group (MUFG). MUFG successfully purchased 20.1% of the shares in Danamon for IDR17.18 trillion to secure a controlling stake of 40% of the shares.

The acquisition of PT Prima Top Boga by PT Nippon Indosari Corpindo Tbk. (Sari Roti) also made an impact on the Indonesian market not because of the size of the transaction but because the KPPU imposed a fine of IDR2.8 billion on Sari Roti due to its failure to submit the mandatory merger report to KPPU. This shows KPPU's seriousness in monitoring compliance with the merger reporting regime in Indonesia.

LEGISLATION AND POLICY CHANGES

Indonesia has quite a unique and complex regulatory and government monitoring system. There are many layers of regulations depending on the type of business, nature of investment, company status (private or public) and geographical location (central or regional). The government supervisory authorities are also divided depending on the business characteristics. For example, foreign investment in Indonesia is subject to the BKPM's regime, while specific types of businesses, particularly in the banking and non-bank financial institution sectors as well as public companies, fall within the authority of the Financial Services Authority of Indonesia (Otoritas Jasa Keuangan – OJK). In addition, regional governments also have specific authorisations for specific activities.

The key regulation applicable to all M&A transactions involving limited liability companies, regardless of the type of business, is Law No. 40 of 2007 (and its implementing regulations) concerning limited liability companies.

M&A relating to foreign investment/foreign investment companies is furthermore subject to the rules and regulations of Law No. 25 of 2007 (and its implementing regulations) concerning investments, as well as the rules and regulations issued by the BKPM. The BKPM also recently issued Regulation No. 6 of 2018 concerning Guidelines and Procedures for Investment Licensing and Facilities (BKPM Regulation 6).

Public companies, bank and non-bank financial institutions are subject to the regime of the OJK and specific OJK regulations, depending on type of activities.

Recent changes in law

There are two significant regulatory updates that have had an impact on M&A transactions. These are the new Government Regulation No. 24 of 2018 on Electronically Integrated Licensing Services and BKPM Regulation 6. Since the issuance of these regulations, investment and business licences are now obtained electronically and integrated through the OSS System rather than through the manual applications in the past.

Regulatory changes

The government of Indonesia is looking at amending the current Indonesian Investment Negative List to allow full foreign ownership in a greater number of business sectors.

Furthermore, the OJK seems to be looking at relaxing the so-called Single Presence Policy provision for banks, which currently limits a shareholder to the control of only one Indonesian bank (with certain exemptions under specific circumstances).

Finally, practitioners are now expecting the new Anti-Trust Law to be enacted in 2019 (after several years' postponement). One significant change in this law would be the amendment of the merger notification requirement from post-notification to prior approval.

MARKET NORMS

There are certain issues that come up with regards to market practice. A different interpretation and understanding of certain regulatory requirements between practitioners leads to the common mistake of missing crucial regulatory requirements for an M&A transaction. Notable examples include the announcement requirements for any change of control and the requirement to sign a deed of transfer of shares in a notarial deed and in the Indonesian language.

Frequently overlooked areas

Corporate governance is the most overlooked issue, particularly in relation to the preparation of a shareholders' register or an acquisition announcement.

PUBLIC M&A

Obtaining control of a public company can be conducted either by acquiring the existing controller's shares or by purchasing shares through a rights issue (capital increase).

Change of control occurs when a party (i) acquires more than 50% of the shares in the public company, or (ii) acquires fewer than 50% of the shares but can influence or determine, directly or indirectly, the management and/or policies in the public company.

An acquisition of shares from an existing shareholder will trigger a mandatory tender offer (MTO) if there is a change of control, with certain exemptions set by the regulations. The MTO may further trigger a re-float obligation if the MTO causes the controlling shareholder to obtain more than 80% of the public company's shares. A voluntary tender offer (VTO) and merger are also ways to obtain control. However, these structures are less popular since a VTO is often used for delisting and privatisation and due to the intricateness of a merger.

Conditions for a public takeover

In an MTO the acquirer undertakes that the existing shareholders (minority shareholders) receive a fair price for their shares in accordance with the provisions of the regulation. Post-merger notification is also a condition.

Break fees

Break fees are not regulated under Indonesian law and the arrangement is purely a contractual matter.

PRIVATE M&A

The tools and techniques used in private M&A really depend on the characteristics of the business of the target and the negotiating circumstances of the parties.

A locked-box mechanism is more common for transactions that involve companies with dynamic business activities and a wide range of customer portfolios, such as bank or multi-finance company.

An escrow is common for specific deals where certain conditions or procedures are to be fulfilled by the buyer and seller within the same timeframe or in interconnected deals which require payment to be fully paid up/made before the other connected deal is completed or where there is a price adjustment agreed by the parties after the completion.

Another alternative is a price adjustment mechanism, which allows the parties to adjust the purchase price after completion (if, for example, the valuation of the assets/shares decreases).

Conditions for a private takeover

Fundamental pre-closing conditions, depending on the characteristics of the deal and business line, are: government approvals (if required by specific regulations); the internal corporate approval of the parties and acquired company; creditors' consent under the existing agreements; and a newspaper announcement to the creditors and employees.

Post conditions are more administrative requirements by nature and include for example, a notification to the authorised government and the creditors and a newspaper announcement. This includes the merger notification report to the KPPU when the threshold set under the regulation is met. Other contractual conditions between shareholders can include non-competition (between the business of the shareholders and the acquired company) and price adjustment conditions.

It is common to include foreign jurisdiction in the conditional share purchase agreement (SPA), although for the deed of transfer it must be governed by Indonesian law.

The exit environment

In a public company takeover, the new controller is required to make an offer to purchase the remaining shares of the public company through an MTO. The MTO is also an exit for the existing shareholders (minority shareholders) who disagree with the acquisition; whereby their shares will be purchased at a fair price by the new controller.

In addition, Indonesian company law provides a right to shareholders to request the company to conduct a shares buy-back if the shareholder(s) disagree with, among others, the merger, consolidation or acquisition on the basis that it causes losses to the shareholder(s) of the company.

OUTLOOK

Key areas of activity in terms of trends and development will most likely involve the consumer goods services, multi-finance providers and tech-related sectors. In multi-finance, the OJK just issued a new regulation liberating some areas for multi-finance companies, which we expect will stimulate M&A involving multi-finance companies.

About the author |

||

|

|

Luky I Walalangi Founder and managing partner, Walalangi & Partners Jakarta, Indonesia T: +62 21 5080 8600 F: +62 21 5080 8601 Luky Walalangi is an Indonesian qualified lawyer and an expert and a leading lawyer in M&A, banking and finance and real estate transactions with over 17 years' experience. Luky has recently been assisting various foreign companies in their complex investments and acquisitions and portfolio loans acquisitions, real property projects and corporate restructurings in Indonesia. He has represented leading global banking and financial groups on major finance transactions, bond issuances and sophisticated fund raising projects, as well as number of major electricity projects in Indonesia. Luky is regarded by Chambers Asia Pacific as a Leading Individual in Corporate/M&A, by IFLR1000 as Leading Lawyer, by Asialaw Profiles as one of five best lawyers in Indonesia. Asia Business Law Journal lists him as one of the A-List Indonesia's Top 100 Lawyers. |

About the author |

||

|

|

Miriam Andreta Partner, Walalangi & Partners Jakarta, Indonesia T: +62 21 5080 8600 F: +62 21 5080 8601 Miriam Andreta is an Indonesian qualified lawyer and expert in M&A, banking & finance, oil and gas and antitrust matters. She has 13 years' experience acting for both foreign and domestic lenders in high profile syndication financing to Indonesian companies. She also represents reputable foreign investment companies in upstream and downstream oil and gas projects and multinational companies in their investments Indonesia, as well as Indonesian state-owned companies on various legal matters. Miriam has advised both local and foreign companies on various antitrust issues. Miriam was one of the top five finalists in the Young Lawyer of the Year category, nominated as Woman Lawyer of the Year and also listed as "40 Under 40" in ALB Indonesia Law Awards 2018. |

About the author |

||

|

|

Renansyah Jenie Associate, Walalangi & Partners Jakarta, Indonesia T: +62 21 5080 8600 F: +62 21 5080 8601 Renansyah Jenie is a bright and agile lawyer with four years' experience in Indonesian legal practice involving both domestic and cross-border markets. He graduated from the Faculty of Law, University of Padjadjaran. He has assisted clients on various transactions of banking and finance, capital markets, M&A, foreign direct investment and general corporate matters, including foreign companies in their complicated financing structures, capital market transactions, M&A schemes and investment plans. |