Prior to the Covid-19 pandemic the Vietnamese M&A market had, as with the economy, remained buoyant. Although 2021 was economically a relatively muted year with only 2.5% GDP growth, it remained an incredibly robust year for M&A transactions (which mirrored 2021 global activity).

The use of Vietnam as an alternative in the ‘China plus One’ strategy being adopted remains a hot topic that is expected to benefit Vietnam, with other talking points being the implementation of recently adopted trade agreements (specifically the EU-Vietnam Free Trade Agreement, the UK-Vietnam Free Trade Agreement, and the Regional Comprehensive Economic Partnership). There is also a general buzz surrounding Vietnamese companies exploring offshore IPOs (along a similar path that Chinese companies had previously taken).

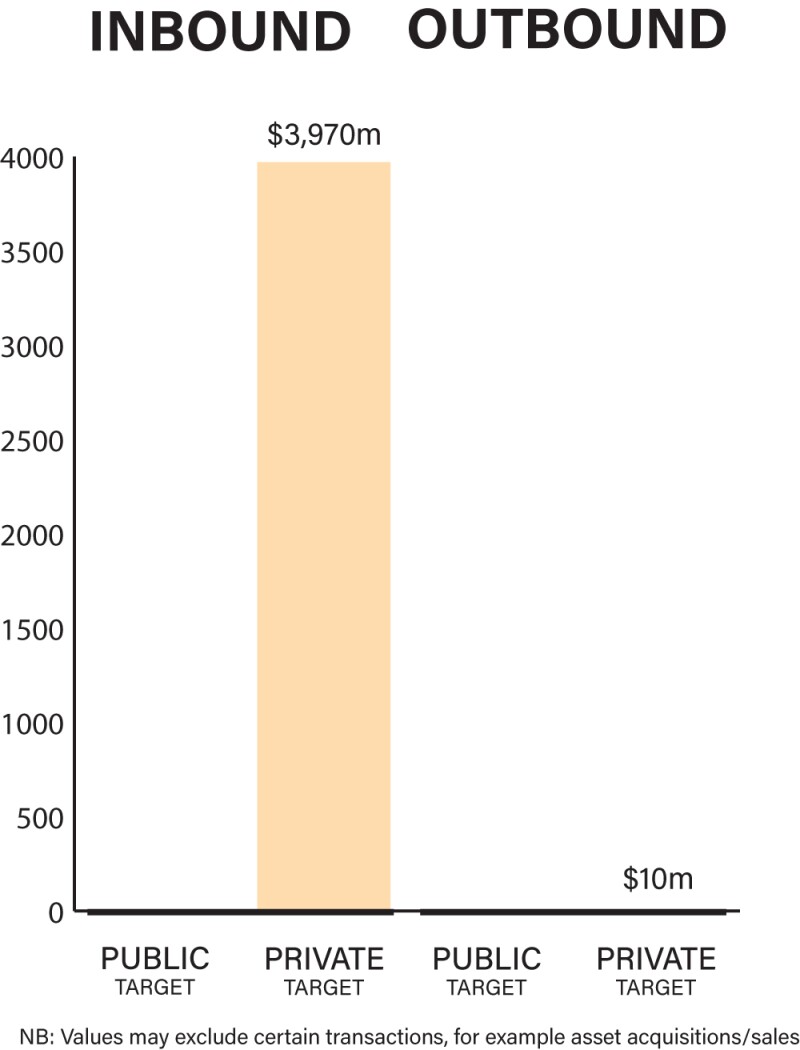

There is strong activity in both private and public M&A in Vietnam. Naturally, there are more private M&A transactions and as with other markets, it is the case that listed companies drive private M&A activity.

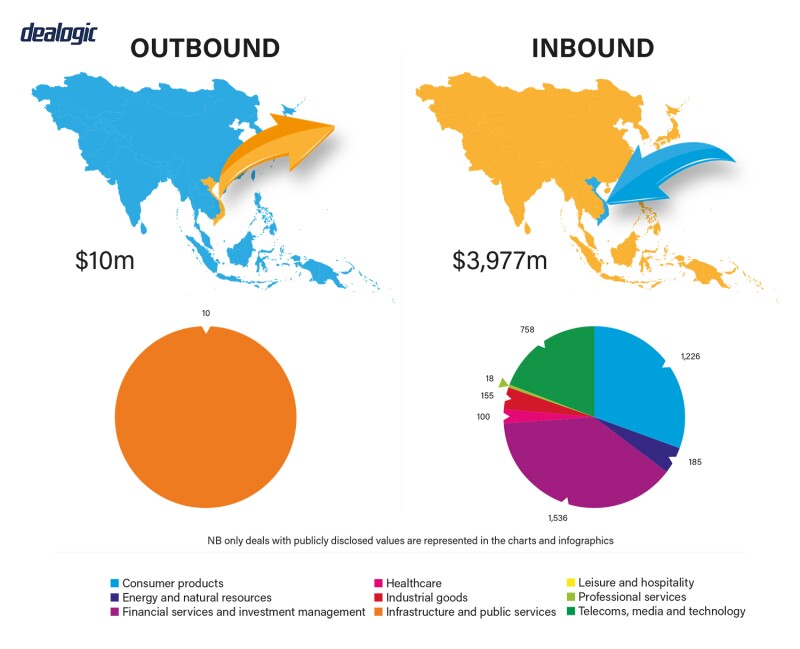

SMBC Consumer Finance (Japan), an affiliate of SMBC Consumer Finance, acquired a 49% of stake in VPBank Finance Company Limited, the finance company of Vietnam Prosperity Joint Stock Commercial Bank (VPBank) for a reported value of up to $1.4 billion.

The deal shows the increasing attention paid by foreign investors in the fast-growing Vietnam consumer finance sector, and it is likely to be the largest investment by a Japanese organisation in the Vietnamese banking sector and the largest M&A deal in the sector to date. Another consumer finance-related transaction is the sale by Saigon-Hanoi Commercial Bank (SHCB) of its 100% stake in its financial consumer arm, SHBank Finance Company Limited, to Bank of Ayudhya Public Company (Krungsri) (Thailand) for a reported $156 million.

In both deals, YKVN acted as the counsel to sellers. Another significant deal, also involving YKVN, was the acquisition by a consortium led by Alibaba Group and Baring Private Equity Asia of a 5.5% stake of CrownX Corporation (CrownX) for $400 million. This transaction valued CrownX, which is a retail consumer platform that consolidates the conglomerate Masan Group’s interests in Masan Consumer Holdings and VinCommerce, at $6.9 billion. CrownX aims to enhance the offline and online marketplace in Vietnam.

Economic recovery plans

As a result of the Covid-19 pandemic which saw stricter restrictions during 2021, Vietnam’s economy grew at a much lower rate then the previous decade, though it should be noted that Vietnam mustered growth whilst other countries saw negative growth when undergoing a similar experience. Despite the low growth rate, 2021 was an incredibly good year for M&A in Vietnam and the market did not go against the global trend, following on from a successful 2020.

It is expected that Vietnam will experience significant M&A activity in 2022. Amongst the reasons for this are that Vietnam continues to offer a safe and stable investment environment, more so with prevailing geopolitical tensions. Multinationals continue to develop their supply chains within Vietnam. Foreign direct investment (i.e. inbound activity) will remain highly significant and 2021 actually saw an increase in value in foreign direct investment (though the number of investments did decrease).

|

|

“Financial investor influence in the market is expected to grow through 2022 and beyond” |

|

|

Deal flow will also be attributed to the increasing pace of domestic activity (by Vietnamese corporates) as well as increasing domestic demand. Discreet changes being experienced will also drive investment, such as the practical timeframes for various approvals lessening and the increasing sophistication of local services being offered.

To round off, the biggest indicator of increased deal flow is that Vietnam’s economy continues to grow year on year and if 2021 delivered a massive M&A year with lower growth than we expect a buoyant 2022 where expectations are that a 6.0% and upwards growth rate should be achieved.

Despite Covid having an impact, deal structures have not changed significantly. Significant distressed transaction are uncommon, though transaction terms around Material Adverse Change (MAC) and Force Majeure Clauses have become more common. Specific indemnity and post-closing price adjustments have also become more common.

Investment fund activity in Vietnam continues to increase, including sovereign wealth fund interest with both the Abu Dhabi Investment Authority and Temasek (the Singaporean sovereign investor) participating in the investment into CrownX described earlier. In 2020, KKR was involved in a blockbuster investment into Vinhomes (reported at $650 million) and followed in 2021 with a reported $100 million investment into education group EQuest Education. Financial investor influence in the market is expected to grow through 2022 and beyond.

Legislation and policy changes

In Vietnam, the key laws that govern M&A activity are the Enterprise Law, the Investment Law, the Securities Law, and, also important, the Competition Law. While the Enterprise Law regulates enterprises (akin to company law elsewhere), the Investment Law regulates investments in projects and business lines in Vietnam. These two laws are, broadly, regulated by the Ministry of Planning and Investment and administered through a local Department of Planning and Investment or local industrial zone management authority.

The Securities Law governs the securities market and operations of public companies, with the State Securities Commission (SSC) as the regulator. The Competition Law remains relevant and is directed by the National Competition Commission (NCC). The establishment of the NCC is yet to occur and, presently, the competition law remains administered by the Vietnam Competition and Consumer Protection Agency (VCA). The VCA is essentially developing practice policy in respect of the new Competition Law (in effect from January 1 2021) and it remains possible that the NCC may have a different approach (though there is nothing to indicate that there would be a marked difference in approach).

Each of the key laws is a very recent iteration of its predecessor. The Law on Enterprises (2020) has, among others, introduced greater shareholders’ rights. As an example, the requirements for shareholders to call a meeting have been softened and shareholders need only hold 5% of the issued voting shares (previously 10%) for no period of time to do so (previously a six-month threshold applied). Additionally, 75% of holders of non-voting preference shares must now approve any matter that may adversely impact their rights and obligations as holders.

Under the Law on Investment (2020), the requirement for foreign investors to obtain approval to invest (the so-called ‘M&A approval’) has been narrowed. For example, if there is a change of foreign shareholder, but no increase in the shareholding percentage held by any foreign shareholder, then no M&A approval is required.

Separately, the new law expands the beneficiaries that may receive investment incentives. Newly added groups are (i) start-up projects, and (ii) small and medium-sized enterprises engaged in certain business sectors (for example, incubators and technical establishments). Forms of incentives include, among others, corporate income tax incentives, exemption from import tax on goods imported to form fixed assets, exemption or reduction in land levies, or land rental. A recent change in law has resulted in the management boards of industrial and specialised zones being empowered to grant M&A approvals (if required).

The new Securities Law 2019 has heightened IPO, corporate governance, and disclosure requirements. To pursue an IPO, a public company must now have charter capital (akin to share capital) of VND30 billion (approximately $1.3 million), an increase from VND10 billion (approximately $430 thousand).

The SSC has also applied a set of best practices of corporate governance for listed companies, which are based on the OECD standards, and a comprehensive set of disclosure requirements applicable to public companies and their substantial and related person shareholders.

Merger filings have become a more prevalent issue when a purchaser acquires control. Thresholds for a merger filing – and therefore merger clearance – are not set at particularly high values. If the control test of transactions in Vietnam is met, the merger filing is required where:

The total assets in Vietnam of any party to the transaction (including its affiliates) is equal to VND3,000 billion or more;

The total sales or purchases in Vietnam of any party to the transaction (including its affiliates) is equal to VND3,000 billion or more;

The combined market share of parties to the transaction (including their affiliates) in Vietnam is equal to 20% or more; or

If the value of the economic concentration (i.e. the transaction) is equal to VND1,000 billion or more.

Importantly, these thresholds (save for transaction value) also apply to offshore transactions. Recently, Vietnamese competition and tax authorities have been exercising their jurisdiction over offshore transactions in so far as these relate to assets in Vietnam. It can be expected that this policy will remain in place.

Although ESG has not historically featured, greater attention is being paid to it. This does not arise due to Covid-19 and rather simply a trend as the market matures. The Vietnam Corporate Governance Code of Best Practices (adopted in 2019) is itself indicative of a desire to follow best governance practices and ESG forms a part of this broader trend. Renewable energy projects, and the significant M&A activity in this, are part of a greening revolution.

M&A transactions include increasingly stringent environmental compliance terms (mostly in the form of warranties) and, from a governance perspective, more transactions feature anti-bribery and anti-money laundering provisions. There is also an increasing focus on information technology-related governance. More and more acquirers, especially multinational investors, have developed their own scorecard and measurement criteria for addressing ESG risks and opportunities.

Market norms

Vietnam’s regulatory regime, as with its economy, has experienced rapid development over a comparatively short period and, unlike developed jurisdictions, authorities and even lawyers may have different views of the law. Although there remains a strong level of certainty on outcomes generally, the rapid development being experienced may result in problem-solving that differs as compared to “regular” approaches expected by foreign investors. However, fears can be assuaged based on local experience and the sheer volume of increasing FDI is indicative of the confidence that investors have.

Regulatory approvals may require a greater degree of consultation with authorities than expected, though authorities are continuously improving their turn-around times and responsiveness. Furthermore, as each year passes, the level of sophistication of officials improves.

Other frequently asked questions usually relate to deal structuring including foreign ownership restrictions, cash flow and tax-related issues, regulatory approvals, and licensing. Overlooked areas, which need careful consideration, include the time required for completion and sequencing of closing deliverables.

Digital and virtual tools are gaining prominence in M&A transactions, especially due to previous Covid-19 related restrictions. The use of virtual data rooms, virtual meetings, and digital signatures increase efficiency in the diligence and deal-making process.

Public M&A

An acquisition for 25% or more of the issued voting shares of a public company requires that a public tender offer (PTO) be made and registered with the SSC. In addition, a PTO is also triggered where the acquisition of voting shares in a public company results in an existing shareholder directly or indirectly holding at least 35%, 45%, 55%, 65%, or 75% of the voting shares in such public company (i.e., where already holdings 25% or more). The bidder must register the PTO with the SSC, then, publicly announce the PTO as prescribed under laws. The target board is required to deliver its opinion of the PTO to shareholders and the SSC.

Therefore, although Vietnamese law does not apply a takeover regime that distinguishes between friendly and hostile takeovers, engagement with the target board remains important. As is the case elsewhere, the duties of directors become important in the context of a hostile takeover. In addition, if the bidder acquires 80% or more of voting shares of a public company, it must make a compulsory offer to buy the shares of the remaining shareholders (on the same terms as the PTO).

The offer can only contain basic and standard transaction terms, such as the total number of purchased shares, minimum purchased shares, offer price, offer period, payment method, and the circumstances that the offer can be withdrawn. In so far as conditionality is concerned, a bidder may only withdraw a registered PTO in limited circumstances permitted by law, among others, acceptances of the offer are less than the minimum registered number of shares offered to be acquired, where there is a change in the number of voting shares of the target company, or the company sells its assets valued at least 35% of its total assets. There is no restriction on making a new PTO if the previous PTO fails.

There are no regulations on break fees, being governed only by agreement. In practice, break fees are occasionally used, and reverse break fees are even less common. The range is usually 1-2% of the transaction value. The enforceability of break fees and reverse break fees are generally untested.

Private M&A

Pricing structures are usually simplistic, though more complex price mechanisms do occur. Locked box mechanisms are more commonly used for majority acquisitions, whilst completion accounts are used more often for minority acquisitions. Earnouts and other forms of deferred consideration are not typical. Escrow accounts are utilised and it is not unusual for sellers to request a deposit payment. Warranty and indemnity insurance remain uncommon.

Private offers are usually subject to regulatory or licensing conditions, along with corporate governance rights by way of provisions of constitutional documents. It is not unusual for a MAC condition to be included, though Covid-19 has resulted in negotiation on MAC clauses to exclude the impacts of the pandemic and the shifting of risk from closing to signing to avoid walk-aways. In several instances, signing and closing occur almost simultaneously or the time gap between signing and closing is relatively short with fewer conditions precedent.

It is not unusual, where a foreign party is involved, for purchase agreements to be governed by Vietnamese law and referred to the Vietnam International Arbitration Center. For a high-value or complex deal, this is usually accompanied by a foreign choice of dispute forum (in particular foreign arbitration). The typical combination is Vietnamese law and the Vietnam International Arbitration Center or the Singapore International Arbitration. Vietnam is a member of the New York Convention and Vietnamese courts are increasingly enforcing foreign arbitral awards and judgments.

Most exits in Vietnam are carried out through trade sales and secondary buyouts (sales to financial sponsors). Unlike the global trend, IPOs within Vietnam have not occurred in large numbers in recent years notwithstanding the growth in the investor base in the capital markets. Vietnamese companies have at times contemplated offshore IPOs.

Looking ahead

We believe that Vietnam will experience significant M&A activity in the Year of the Tiger (2022). This follows the trend set in 2021 and in an environment with higher GDP growth and the lifting of Covid-related restrictions.

Although geopolitical tensions may result in global headwinds, we believe that Vietnam remains somewhat insulated (although acknowledging that this may impact Vietnam’s export markets). As M&A practitioners, we foresee increasing complexity and sophistication of both local transactions and clients, as has been the recent trend.

Truong Nhat Quang

Managing partner

YKVN

T: +84 28 3822 3155

About the author

Truong Nhat Quang is the managing partner of YKVN. He heads a well-recognised, top tier corporate practice focused on banking, M&A, private equity, and capital markets transactions.

Quang has successfully handled landmark deals in Vietnam, regularly advising on complex M&A transactions and private equity investments as well as representing international banks, multinational investors, government agencies, and multilateral organisations on nation-shaping industrial transactions and projects. His clients include top Vietnamese banks and corporates, global investment banks, banks active in Vietnam and global private equity funds.

Quang has authored the treaties on Vietnamese contract law and corporate law, while also authoring guidance on skills for transactional business lawyers. He is a graduate of Hanoi University of Law.

Le Thi Loc

Partner

YKVN

T: + 84 28 3822 3155

About the author

Le Thi Loc is a partner in YKVN’s Ho Chi Minh City office. With over 20 years of experience, her practice focuses on M&A, real estate, foreign investment, and corporate matters.

Loc regularly assists foreign investors on commercial and investment activities in Vietnam, from the pre-licensing to the post-licensing stage. Highly active in M&A, she has advised leading local companies, state-owned enterprises, major Vietnamese conglomerates, multinational corporations, and private equity funds. In addition, she is an expert on logistics, employment, fintech and e-commerce practice and education.

Loc completed her bachelor’s degree at Hanoi University of Law and her LLM at University of California, Berkeley School of Law.

Nguyen Ngoc Bich Tram

Partner

YKVN

T: +84 28 3822 3155

About the author

Nguyen Ngoc Bich Tram is a partner of YKVN’s Ho Chi Minh City office. Her practice focuses on corporate M&A (especially in real estate, healthcare, education, pharmaceutical business and distribution), foreign investment, and other commercial and corporate matters.

Tram has participated in various fund raising transactions involving Vietnamese companies. She has acted as legal counsel to multinational corporations, local companies, and private equity funds. She also specialises in providing advice on education, corporate, investment, fin-tech and e-commerce.

Tram has a law degree from Ho Chi Minh City University of Law, and a LLM from University of the West of England.