Marcus Peter, GSK Stockmann (Luxembourg)

MARKET OVERVIEW

2018 has once again shown a growing trend in M&A transactions with a view to Luxembourg-based target entities as well as acquisitions outside of Luxembourg that were started using a Luxembourg structure. Luxembourg-based targets are typically not the centre of high-profile M&A targets.

The last large M&A transaction with a Luxembourg target entity was the approximately €30 billion ($34 billion) successful takeover bid for Mittal Steel by Arcelor, which resulted in the biggest steel producing entity worldwide. Other local M&A transactions were the investment by Qatar into Cargolux, a worldwide leading cargo airline operating from Luxembourg, and their investment into KBL Bank or Banque Internationale à Luxembourg, as well as other investments by Qatar and Chinese investors into Luxembourg-based banks and asset managers. Another transaction was the sale by Lufthansa of its stake in the Luxembourg civil airline Luxair. Two of the most recent transactions involving a Chinese investor acquiring a Luxembourg-based targets were the acquisition of the Banque Internationale à Luxembourg by the Legend Holdings Group from Precision Capital (Qatar); and the acquisition of a 25% stake in Encevo by the China Southern Power Grid group.

Hence, Luxembourg is seeing a growing M&A volume with targets located in the country and it continues to remain a core jurisdiction in the EU as a hub from which M&A transactions are guided into other European jurisdictions. A large portion of the M&A transactions in Europe and also in relation to other continents (in particular Asia) are implemented by using Luxembourg structures. Over the last years Luxembourg also has experienced a growing interest from China-based investors in carrying out their M&A transactions in the EU or Latin America via Luxembourg investment structures.

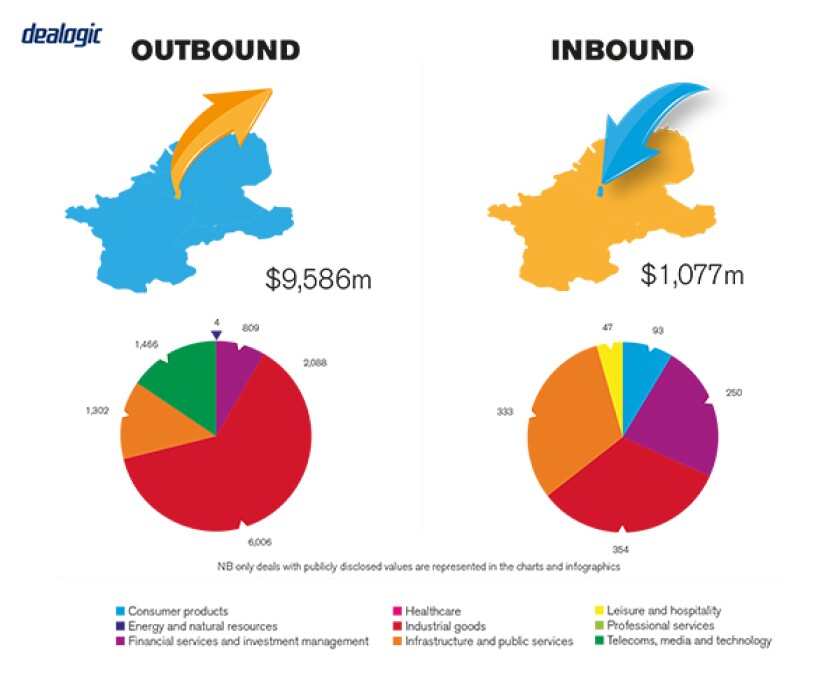

No official figures as to volume and value of M&A deal flow in Luxembourg are available for 2018. However, during the last 12 months the assets under management (AUM) of private equity (PE) buy-out funds has strongly risen in Luxembourg. It is estimated that around €75 billion of AUM were committed in 2018 and fundraising is ongoing for additional multi-billion euro PE funds in Luxembourg. These funds have been investing and will further deploy M&A transactions aimed at mostly European-based target entities. The outlook for M&A activity in and directed from Luxembourg remains very good.

M&A activity

There has been no real difference to previous years. Sectors of M&A activity remain diverse. The deal volume for Luxembourg itself remain rather small, however M&A deals steered through Luxembourg vehicles into other markets remains high.

The market is characterised by a mix of private and public M&A transactions. Again, the target of both is often not located in Luxembourg itself but in other jurisdictions. Due to the positive legal and business environment in Luxembourg we often see M&A transactions with European targets orchestrated from a Luxembourg-based structure (investment fund or other).

TRANSACTION STRUCTURES

As well as the deals mentioned above, transactions managed through Luxembourg structures and with targets in other countries are numerous. In particular, acquisitions of German, Italian, Swiss, Spanish, Portuguese and French target entities seem currently to be predominantly carried out through Luxembourg investment structures. It was reported that the M&A transaction into Pirelli had a Luxembourg element, as well as the investment into the Kuoni Travel Group and the acquisition of the Building and Facility Management segment of Bilfinger.

Financial investors

Strategic and financial investors alike use Luxembourg as an M&A hub to approach target entities in Luxembourg or abroad. These investor groups are increasingly choosing Luxembourg as their investment platform. This is due to the stable and investor-friendly business environment for which Luxembourg is well-known in the global investor and asset manager community. The flexible investment fund and corporate law regime allows for tailor-made solution for all kinds of investment platforms and asset classes. Furthermore, the multi-linguistic workforce in Luxembourg (private and public sector) allows investors to communicate with their advisors, administrators and even the supervisory authority in English, German or French. Advisory firms typically also have native speaking staff in Luxembourg to serve many other countries worldwide, in particular China, Russia, Middle East and Latin America.

LEGISLATION AND POLICY CHANGES

The key legislation is the law on commercial companies dated August 10 1915, as amended (Corporate Law). The Corporate Law provides for all kinds of corporate structures and corporate instruments to create tailor-made structures useable for M&A transactions. In addition, numerous treaties on the avoidance of double taxation allow Luxembourg to support the worldwide M&A activities of Luxembourg PE funds and M&A interested parties.

Another key piece of legislation is the Takeover Law of May 19 2006, as amended (Takeover Law). The Takeover Law includes squeeze-out and sell-out rights, which assist M&A activities involving Luxembourg target entities. Any voluntary bid for the takeover of a Luxembourg company and any mandatory bid will be subject to the Takeover Law, which implemented EU Directive 2004/25/EC of the Council of April 21 2004 concerning takeover bids (the Takeover Directive) into Luxembourg law. A natural or legal person acquiring, alone or with persons acting in concert with it, control over a company by holding 33 1/3 % of the voting rights is required to make a mandatory takeover bid to all the holders of shares in the Luxembourg company. As far as the competent authority is concerned, the Takeover Law states that if the target company's securities are not admitted to trading on a regulated market in the EU member state in which the company has its registered office, the competent authority to supervise the bid will be the authority of the member state responsible for the regulated market on which the company's securities are admitted to trading.

Matters relating to the consideration offered in the case of a bid, in particular the price, and matters relating to the bid procedure, in particular the information on the bidder's decision to make a bid, the content of the offer document and the disclosure of the bid are governed by the law of the member state responsible for the regulated market on which the company's securities are admitted for trading. If a mandatory or voluntary offer is made to all of the holders of securities carrying voting rights in a company, which has its securities listed on a regulated market and if, after an offer, the offeror holds 95% of the securities carrying voting rights of the respective company and 95% of the voting rights, the offeror is entitled to squeeze-out the minority shareholders according to the provisions of the Takeover Law.

Under the Takeover Law, when a mandatory or voluntary offer is made to all the holders of securities that carry voting rights in a company and if, after the offer, the offeror holds more than 90% of the securities carrying voting rights and more than 90% of the voting rights, the minority shareholders may require that the offeror purchase the remaining securities in the same class. Finally, the law of July 21 2012 governing the mandatory squeeze-out and sell-out of securities of companies currently admitted or previously admitted to trading on a regulated market or having been offered to the public (the Luxembourg Squeeze-Out and Sell-Out Law) governs the squeeze-out and sell-out of minority shareholders of a company that has its registered seat in Luxembourg by a majority shareholder. The Luxembourg Squeeze-Out and Sell-Out Law applies if all or part of a company's securities are: (i) currently admitted for trading on a regulated market in one or more EU member states; (ii) no longer traded, but were admitted for trading on a regulated market and the delisting became effective earlier than five years ago; or (iii) were the subject of a public offer which triggered the obligation to publish a prospectus in accordance with the Prospectus Directive or, if there is no obligation to publish according to the Prospectus Directive, where the offer started during the previous five years. The Luxembourg Squeeze-Out and Sell-Out Law does not apply during, and for a certain grace period after, a public takeover that is or has been carried out pursuant to the Takeover Directive.

Recent changes in law

The Corporate Law was recently amended to further enhance corporate structuring. It now provides for yet better structuring of share classes and characteristics (voting or non-voting shares / shortening of the period for exercising preferential subscription). New corporate forms were also created, as well as more flexible provisions pertaining to the issuance of bonds and the holding of shareholders general meetings. In addition, new investment fund forms were created (for example the unregulated reserved alternative investment fund or RAIF), which provides for the swift establishment of PE and other alternative funds to allow a period to market investment activity. Recently, there has also been an increase in specialised investment funds (SIF), given the Luxembourg financial supervisory authority (CSSF)'s approval process for a SIF was accelerated.

Furthermore, at the end of 2018 the law on the beneficial owner register was finally passed. The requirements rely on the respective European directive and the register will help to create more transparency on beneficial ownership in Luxembourg entities. This is to the benefit of M&A transactions and should not be an obstacle to progress such transactions.

Regulatory changes under discussion

As well as in other EU jurisdictions, Luxembourg is currently implementing several European-based legislations. Mifid II has already been implemented and the most recent EU directive on know-your-customer (KYC) and anti-money laundering (AML) has been transposed into Luxembourg law.

MARKET NORMS

To our knowledge there are no common mistakes or misconceptions about the Luxembourg M&A market.

Frequently overlooked areas

Common questions relate to the best choice of PE fund vehicle for an M&A activity. Tax is always an important element when setting up a structure. The structure needs to be tax compliant, serve the interest of the investing group and target entity and take into view the upcoming legislative initiatives of the European Union in this regard. Any changes proposed by the European Commission to tax regimes applicable to M&A structuring must not treat one EU member state in an unjustified manner while other EU member states continue to implement unreasonable tax rules. From the perspective of Luxembourg, a more unbiased approach by the European Commission would be welcomed. In this context, the European Commission should not completely suppress tax competition amongst EU member states given the growing pressure from the UK and the US in lowering their tax rates.

PUBLIC M&A

Key factors for public M&A involve complying with the provisions of the Takeover Law. This includes complying with the notification and reporting requirements under the law as well as with other elements related to the activity. In particular, parties to an M&A need to assess how the managing bodies of the takeover target are to be approached and what governmental authorities need to be notified. It is important to draw a line between the jurisdiction of registered office of the target entity and the jurisdiction where the shares are listed on the regulated market. In Luxembourg, the registered office and administrative seat of the target is often located in Luxembourg; however, the shares are admitted for trading on a regulated market other than the Luxembourg Stock Exchange. Hence, the legal impact of such a discrepancy must closely be analysed before any public takeover bid is launched.

Conditions for a public takeover

The main conditions and features are covered by the comments above.

Break fees

The current market practice in Luxembourg shows that break fees are regularly negotiated at the beginning of a transaction. This is common in Luxembourg and it is also accepted by Luxembourg service providers that a break fee can include a certain discount given the economic downside of an unsuccessful bid.

PRIVATE M&A

There are no new current trends in private M&A structures. The concepts mentioned above also apply to Luxembourg private M&A transactions. Completion accounts need to be presented and they may be audited or not. The locked-box mechanism might see a minimum period of six months and go up to two years. Recently, a growing number of private M&A activities can be seen with view to financial sector entities such as alternative investment fund managers or banks. This is yet another sign of the attractiveness of Luxembourg as financial centre in Europe.

Conditions for a private takeover

Typically, no specific provisions for a private takeover offer exist. The Corporate Law provisions apply, as well as the constitutive documents of the privately-owned target entity. A shareholders' agreement will most likely also be in place which will contain provisions pertaining to drag-along, tag-along and pre-emptive rights.

Foreign governing law

Share purchase agreements involving Luxembourg-based target entities are typically drafted under and made subject to Luxembourg law. English law is also used on certain occasions, however especially due to the current Brexit negotiations clients seem to query the risks and necessity of using English law (for private M&A transactions and in general for legal documents). This has given Luxembourg law a certain growing dominance in legal agreements for Luxembourg-related transactions.

The exit environment

Exit strategies remain the standard ones. We do see IPOs and they are often prepared as an exit strategy, however a sale is then often preferred over an IPO. Sales to strategic sponsors are rare, however sales to or amongst PE firms are seemingly increasingly common.

OUTLOOK

The outlook is positive for 2019. We expect a growing number of M&A transactions in Luxembourg itself, however even more important for M&A transactions launched from Luxembourg vehicles into other EU jurisdictions. The tightening of Chinese regulations on outbound M&A we saw in 2018 has now been relaxed and we are again expecting growing M&A activity from China via Luxembourg into other EU member states and into Latin America.

About the author |

||

|

|

Marcus Peter Position equity partner, GSK Stockmann (Luxembourg) Luxembourg T: +352 2718 0200 F: ++352 2718 0211 Web: www.gsk-lux.com Marcus Peter heads the investment funds and private equity practice at GSK Stockmann Luxembourg. Marcus is a lawyer qualified to practice in Germany since 2004 and Luxembourg since 2005. He obtained his LLM and PhD degrees from the European Institute in Saarbruecken, Germany. Prior to joining GSK Luxembourg, Marcus worked for a Luxembourg law firm from 2004-16, spending the last four years as a partner). He has been a partner at GSK Stockmann in Luxembourg since 2016. Marcus is an expert in Luxembourg investment funds & private equity law, M&A and corporate law. He speaks German, English, French and Russian. He is a member of the Luxembourg Private Equity Association (LPEA), Chinese-Luxembourgish Chamber of Commerce, DAV Luxembourg, EVER and CBBL (Cross Border Business Lawyers). |