Roddy Martin and Antonia Kirkby, Herbert Smith Freehills

MARKET OVERVIEW

As we look ahead in 2019, after a strong year in 2018, the M&A environment is less certain due to the political uncertainty around Brexit and the associated possibility of an economic slowdown. However, there are several factors that indicate we may see continued M&A activity, including the weakness of the pound which should continue to attract bidders to UK targets. We also expect end-of-cycle factors to lead to boards offloading non-core assets and increased pressure from activists.

M&A activity

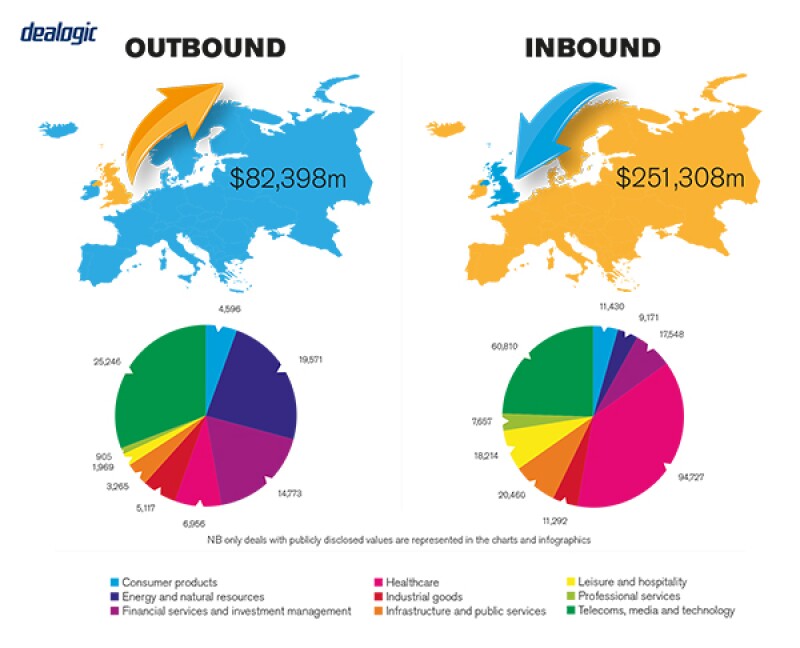

M&A activity in 2018 continued to be strong in the UK. While the number of deals was broadly the same as the previous year, we saw in particular a good number of mega deals, with more public transactions over £1 billion (approximately $1.29 billion) in 2018 than 2017.

We did however see a slowdown in the second half of 2018, perhaps as a result of Brexit and the associated uncertainty it has given rise to.

US buyers were the top acquirers of UK targets in 2018. Asian buyers are also refocusing on Europe, as the US becomes a harder place for international buyers to conduct M&A.

The strongest sectors for M&A activity were TMT, real estate, financial services, infrastructure and healthcare.

Both public and private M&A are highly active in the UK.

For public M&A, the UK Takeover Code provides a well-established regime which, with a lack of associated litigation, means that conducting a recommended takeover of a UK target can be relatively straightforward.

The private M&A market is also well developed and having English law as the governing law, with the stability and certainty it brings, means that again the UK is a relatively easy place to conduct an M&A transaction.

TRANSACTION STRUCTURES

The availability of cheap debt has helped drive M&A activity, as has the need for companies to evolve and adapt to rapidly changing technology in order to remain competitive in their sector.

As well as corporates pursuing full buyouts, we have seen a rise in "corporate venturing", where companies take a stake in a target.

Auctions remain prevalent and we expect that to continue.

An interesting trend has been an increase in the number of interlopers on M&A deals, where longer transaction timetables are giving third parties more opportunity to emerge with a competing bid for the target or a supervening bid for the bidder.

Financial investors

Investors' influence on M&A activity has been on the rise for some time, driven by activist investors who may agitate for a board to undertake a transaction (for example Whitbread's decision to demerge Costa Coffee) or intervene in a transaction that has been announced, either to block it or to try and force the buyer to pay a higher price for a target, known as "bumpitrage". We expect the influence of activists to continue in 2019.

Private equity (PE) is an important contributor to M&A, both directly and indirectly, with its regular participation in auction processes, but there was reduced UK activity on the part of some of the largest PE houses in 2018.

Recent transactions

The most high profile deal of 2018 was the takeover of Sky by Comcast following a protracted process which began in 2016, when 21st Century Fox announced a recommended offer for Sky. The Fox transaction was referred for further investigation on the grounds of media plurality and this is indicative of the UK Government's increasing willingness to intervene in M&A on public interest grounds. Comcast then announced a competing offer and agreed to give post-offer undertakings in connection with the acquisition to reduce the risk of political intervention in its acquisition. The competing offers were ultimately resolved by a rarely-used auction process under the Takeover Code.

Another high profile deal was the hostile offer for GKN by Melrose. This was the first hostile offer for a FTSE 100 company since the takeover of Cadbury by Kraft in 2010. As on the Sky deal, Melrose agreed to give post-offer undertakings to address political concerns about the deal and this is something we may see more of as buyers seek to minimise the risk of political intervention in a transaction.

LEGISLATION AND POLICY CHANGES

The City Code on Takeovers and Mergers (the Takeover Code), which is administered by the Panel on Takeovers and Mergers, governs public M&A in the UK. It applies where there is an acquisition or consolidation of control of a UK public company which is admitted to a UK market or has its place of central management in the UK.

For listed companies, the Market Abuse Regulation and the Listing Rules may also be relevant, in particular the provisions in Chapters 10 and 11 of the Listing Rules which may require premium listed companies to obtain shareholder approval for a transaction.

Parties will have to consider the merger control regime under the EU Merger Regulation and the Enterprise Act.

Aside from merger control regimes, there is no legislation or regulatory body that underpins private M&A – the key legal framework will be provided by contract law, with the underpinning principle being caveat emptor or buyer beware. The buyer will only be afforded protections which are written into the agreement.

The Companies Act 2006 applies to all UK incorporated companies and they and their advisers should consider any relevant provisions. For example, on public M&A, it sets out the regimes for a scheme of arrangement and for squeezing out minority shareholders following a contractual takeover offer.

Recent changes in law

We have seen an increasing trend towards greater intervention by regulators and the Government in transactions that raise competition or public interest concerns.

The Government has lowered the threshold at which it can intervene in transactions in certain sectors, namely military products, quantum technology and computing hardware. The thresholds were lowered in June 2018 and the Government has already used the powers to intervene in the acquisition of Northern Aerospace by Gardener Aerospace in July 2018. These lower thresholds and the Government's willingness to intervene are likely to lead to longer transaction timetables and parties considering whether to give undertakings to try and address any concerns.

Regulatory changes under discussion

The key development likely to impact M&A is Brexit. However, aside from specific issues such as the regime for merger control, the legal framework for M&A is not expected to change significantly.

The Government is consulting on proposed new powers to intervene in deals on the grounds of national security. The proposed new rules are extremely far reaching and would represent a significant increase in the Government's powers, potentially capturing any transaction or investment, irrespective of sector, size or market share.

MARKET NORMS

With regards to any common misconceptions about UK practice, the UK Takeover Panel and the Takeover Code are often misunderstood by international buyers. Compliance with the Code is not optional and the Panel is a very proactive regulator who should, and expects to be, consulted about issues that arise on a transaction.

It is also unusual to use a true "merger" in the UK where two companies become one. It is more common for one company to acquire the shares in another company (even where it is described as a merger), or for a newly incorporated to acquire the two companies which are to "merge".

Frequently overlooked areas

Early planning in relation to anti-trust and, if applicable, public interest intervention is key.

Parties should focus their due diligence on areas which may carry with them reputational risk, such as GDPR compliance, cyber-security and anti-bribery and corruption.

On public M&A, parties should also understand that they will be held to what they say, be it in an announcement, an interview or in the media.

PUBLIC M&A

A bidder can choose one of two methods to acquire a listed company.

The first is a contractual takeover offer, where the bidder makes an offer to the target shareholders to acquire their shares. Its offer will only be successful if the requisite number of shareholders accept the offer – under the Takeover Code, at least 50% of the target shares must be accepted to the offer.

The second method is to use a scheme of arrangement which is a court-sanctioned procedure. A scheme must be approved by shareholders, with at least 75% in value and a majority in number of those voting passing the relevant resolution. If approved, and the court does not consider the scheme to be unfair, the court will order that all the shares in the target be transferred to the bidder.

The speed with which control can be obtained will be determined in part by the structure used. If the bidder uses a scheme, it may be able to gain full control of the company within 26 days of the publication of the shareholder documentation. Alternatively, on a contractual offer a bidder may obtain majority control more quickly than on a scheme, but it is likely to take longer to acquire 100% control as it will have to use the squeeze-out procedure under the Companies Act to acquire the shares held by any shareholders who do not accept the offer.

Because a scheme process is run by the target it is hard to use a scheme for a hostile bid. A scheme may also be less attractive in a competitive situation.

Conditions for a public takeover

As well as the acceptance condition of between 50% and 90% for an offer, or the requisite shareholder approval being obtained on a scheme, as the case may be, a takeover will usually have conditions relating to merger control clearance, any other requisite regulatory or other clearance, including obtaining the approval of the bidder's shareholders (if required), plus a series of business-related conditions. However the Panel will not permit a condition to be invoked unless it is of material significance to the buyer.

Break fees

The Code prohibits "offer-related arrangements", that is agreements between the bidder and target which impose obligations on the target. This prohibition extends to break fees, and so they are only permitted in the limited circumstances set out in the Takeover Code, for example following a formal sale process (akin to an auction process where a company puts itself up for sale).

It has become more common however to see reverse break fees, where the bidder agrees to pay a target a fee if the transaction fails due to, for example, the bidder not recommending the offer to its shareholders.

PRIVATE M&A

When it comes to consideration mechanisms in private transactions, approximately half of share purchase agreements use a locked-box mechanism for consideration adjustment. It is generally perceived as being more favourable to the seller as it limits the scope for adjustment of the consideration post-completion. The bargaining power of the parties may therefore be a factor in determining which adjustment mechanism is used. Completion accounts may also be used for more complex valuation situations. We are also increasingly seeing a hybrid of the two being used.

Earn outs are more commonly used where key individual sellers are remaining as directors or employees of the target.

An escrow may be used either where some additional consideration may be payable (for example if the net asset value is above a certain level) or where the buyer wants to retain part of the purchase price, in case it has any claims against the seller.

Warranty and indemnity insurance continues to increase in popularity as it becomes cheaper and the cover provided more extensive. PE houses in particular like to use it on disposals and it can be a useful tool to facilitate a transaction which has an unusual element to it.

Conditions for a private takeover

The key conditions will likely relate to any merger control / regulatory consents required for the transaction. The parties will want to keep the conditions to the minimum. If the agreement is conditional, the parties will have to consider whether the warranties should be repeated at completion, and whether the buyer should be entitled to walk away if there is a material change between signing and completion. The buyer is also likely to want to impose restrictions on what a seller can do with the business in the period between signing and completion.

Foreign governing law

Share purchase agreements in the UK are almost universally governed by English law and subject to the jurisdiction of the English courts. English law is often used for transactions with no nexus to the UK because it is viewed as a stable and commercial option.

The exit environment

We are seeing very competitive auctions for good assets but, where the assets are less attractive, the auction process may be more protracted with, in some cases, no buyer emerging at the end of it. The IPO market has become quieter but companies continue to run dual track processes for some assets, where a sale process is run alongside an IPO process to establish which is the preferable option. PE houses remain very active in the UK and this is expected to continue as they have cash to spend. We may see some reassessment of asset values as the M&A boom calms down.

OUTLOOK

Continued uncertainty over Brexit, together with the associated possibility of an economic slowdown, may continue to have a negative effect on UK equity markets, which are an important reference point for corporate valuations and an important source of acquisition currency for corporates.

However, the conditions for continued M&A activity are in place. Corporates with strong balance sheets seeking rationalisation and growth, private equity houses with dry powder to invest and the availability of cheap debt – as well as corporates keen to counter the threat of disruption in their business, including as a result of Brexit – should all fuel activity in 2019.

End-of-cycle factors may also lead boards to seek to off-load non-core assets.

About the author |

||

|

|

Roddy Martin Partner, Herbert Smith Freehills London, United Kingdom T: + 44 20 7466 2255 F: + 44 20 7098 5255 W: www.herbertsmithfreehills.com Roddy Martin has considerable experience of advising on cross-border M&A deals, both inbound and outbound, notably those involving newly-industrialised economies, particularly India and China, with a focus on public takeovers, schemes of arrangement, sell-side and buy-side private auctions and bi-laterals, joint-ventures, buyouts, minority participations and management equity pieces. Roddy is also client relationship partner for a number of FTSE companies and international conglomerates. He is a senior member of the firm's India Executive. Roddy's experience includes advising TUI Travel on its £5.2 billion merger with TUI AG, PA Consulting Group on the controlling investment by scheme of arrangement from The Carlyle Group, valuing PA at $1 billion, Reliance Communications on its proposed $1.6 billion sale of its telecom towers business to Brookfield Infrastructure and United Spirits on its £430 million disposal by auction sale of Whyte & Mackay to Emperador. |

About the author |

||

|

|

Antonia Kirkby Professional support lawyer, Herbert Smith Freehills London, United Kingdom T: +44 20 7466 2700 F: + 44 20 7098 5255 W: www.herbertsmithfreehills.com Antonia Kirkby practised as a transaction lawyer specialising in corporate finance and mergers and acquisitions before becoming a professional support lawyer at Herbert Smith Freehills. Her focus is providing the firm's lawyers with technical advice on company law and M&A issues and analysing new law and regulation. Antonia was secretary to the City of London Law Society Company Law Sub-Committee and to the Sub-Committee's Joint Working Party on Takeovers for a number of years, which involved considering and lobbying on a wide range of company law issues, including changes to the Listing Rules and Takeover Code. She continues to contribute to the Takeovers Working Party and respond on proposed changes to legislation and regulation. She has written a number of articles and contributes to a number of books, particularly on public M&A, market abuse and the listing regime. |