Markus Lauer and Nico Abel, Herbert Smith Freehills Germany

MARKET OVERVIEW

Despite Brexit, disruptive trade disputes, rising regulatory scrutiny (foreign investment as well as merger control) and more volatile stock markets, Germany is still seeing strong M&A activity. However, buyers are starting to become more cautious and are aware of the risks associated with the high prices sellers are still seeking for their assets.

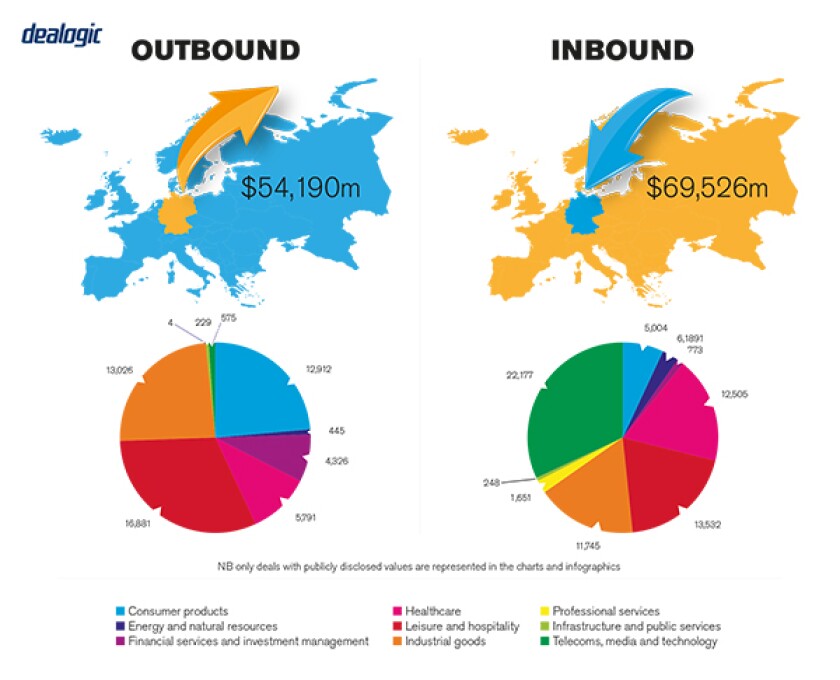

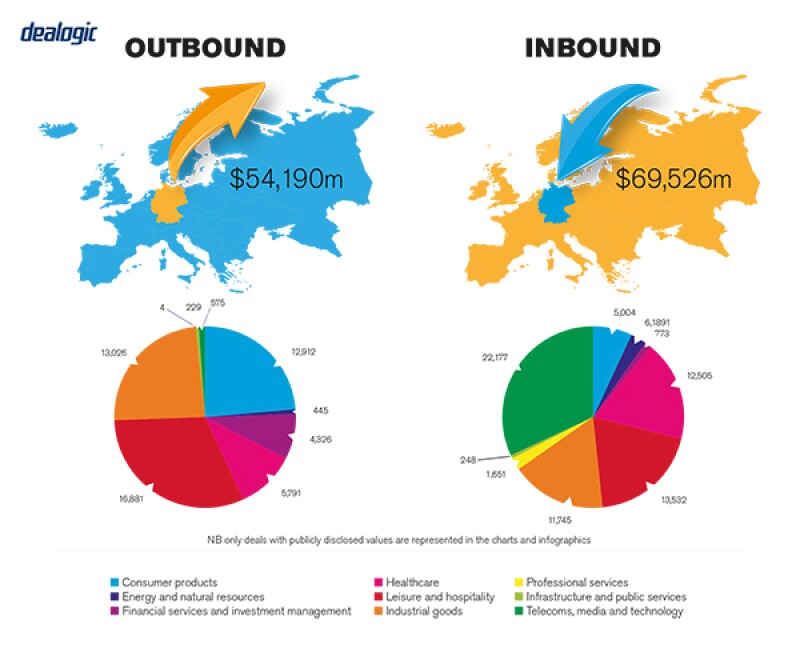

M&A activity

General deal flow has been very strong in the last 12 months. Outbound activity has been driven by German corporates looking to grow their businesses through M&A rather than just by organic growth, in particular into the US. Inbound activity has been fuelled by the strong German economy. On the sellers' side, numerous financial investors have been exiting successful investments while corporates have disposed of non-core assets into the liquid M&A market. On the buyers' side, financial investors have been the most active, as they are still under pressure to invest capital. Chinese investors have recently been less active in the German market.

Generally, M&A has been and will continue to be driven by digitalisation, globalisation, low interest rates and strong liquidity as well as consolidation in industries like real estate, financial services, aviation, energy and chemicals.

The German market is predominantly driven by private M&A. However, the last three to four years have seen an increased number of (large) public M&A transactions compared to earlier periods. These public M&A transactions often fuel private M&A activity, for example through disposals by the parties prior to closing to meet regulatory conditions or post-closing disposals of non-core/redundant assets.

TRANSACTION STRUCTURES

In the current seller-friendly markets, we have seen an increased number of structured auctions with tight timelines and vendor due diligence reports. Alongside that, parties have used the locked-box purchase price concept even more. Finally, warranty and indemnity (W&I) insurance, which was rather uncommon in the German market a few years ago, is now probably an accepted instrument, including stapled solutions in auction processes. It will be interesting whether this continues should the market become less seller-friendly.

Financial investors

In private M&A, the increased use of auctions, vendor due diligence reports, the locked-box concept and W&I insurance (referred to above) has mainly been driven by private equity investors disposing of their assets. Other financial investors, namely activist hedge funds, have recently been targeting German listed companies to challenge their business model and strategy. To a certain degree, this has resulted in disposals as well as spin-offs/split-offs from such listed companies.

Recent transactions

The targeting of ThyssenKrupp by activists is the first time an activist investor has successfully led to a break up of a DAX 30 company. This is a sign of the growing influence of activists, including in the M&A sphere.

LEGISLATION AND POLICY CHANGES

Public M&A activity in Germany has to comply with the German Securities Acquisition and Takeover Act (WpÜG), the German Offer Ordinance and further statutory ordinances, the German Securities Trading Act (WpHG), the Market Abuse Regulation (Marktmissbrauchsverordnung) and the German Stock Corporation Act (AktG). The German Federal Financial Supervisory Authority (BaFin) supervises public takeovers.

On the regulatory side, both for public and private M&A, foreign investments into German companies may be subject to review by the Federal Ministry of Economics (BMWi) in accordance with the German Foreign Trade Act (Außenwirtschaftsgesetz) and applicable ordinances. All industry sectors are in principle subject to cross-sectoral examination, ie the BMWi can, upon becoming aware of a transaction, examine whether it presents a risk to public order or security in Germany. Certain sensitive industries are subject to the so called sectoral-specific examination.

Transactions are subject to mandatory notification to the BMWi where the acquisition may endanger public order or security in Germany (cross-sectoral examination). The legislation contains a non-exhaustive list of companies to which this applies, including companies that operate critical infrastructure in sectors such as energy, TMT, finance, insurance, health and transport; companies which manufacture industry-specific software for such critical infrastructure; providers of cloud-computing; and media companies. During the review period the transaction remains effective. If the BMWi prohibits the transaction after the review, it becomes void from that point and has to be unwound under German civil law. There is technically no requirement to notify and obtain approval prior to completion, although companies may choose to do so before completing for legal certainty, given the risk of the transaction having to be unwound.

Transactions are also subject to mandatory notification to the BMWi where (i) the acquisition relates to a company that manufactures or develops products with military or IT security functions and (ii) the essential security interests of the Federal Republic of Germany are endangered (sector-specific examination). The transaction is ineffective until the BMWi grants its approval.

Both the cross-sectoral and sector-specific rules apply where a foreign investor acquires a German business (the whole company, a branch or a permanent establishment) or a direct or indirect interest of more than 10% in the voting rights of a German business in the case of sectoral-specific cases and certain cross-sectors specified in the German Foreign Trade and Payments Ordinance (Außenwirtschaftsverordnung), or 25% for non-specified cross-sectors but where the acquisition may otherwise endanger the public order or security in Germany. There are no turnover or other monetary thresholds.

Under the German Act against Restraints of Competition (GWB), public and private transactions which constitute a concentration require approval from the Federal Cartel Office (FCO), even if only non-German entities are involved. A transaction that is deemed a concentration is subject to merger control in Germany where in the financial year preceding the transaction: the combined aggregate worldwide turnover of all participating undertakings was more than €500 million (approximately $564 million), the domestic turnover of at least one participating undertaking was more than €25 million, and the domestic turnover of at least one other participating undertaking was more than €5 million. In 2017, an alternative "size of transaction test" was introduced, which is where in the financial year preceding the transaction the combined aggregate worldwide turnover of all parties concerned exceeded €500 million; one party concerned had a turnover in Germany exceeding €25 million; neither the target nor another party had a turnover in Germany exceeding €5 million; the value of consideration for the transaction exceeded €400 million; and the target is active in Germany to a significant extent. German merger control does not apply if an exemption applies (for example if the transaction will have no local effect); or a concentration falls into the scope of the EU Merger Regulation.

Recent changes in law

In July 2017, an amendment to the German Foreign Trade and Payments Ordinance (Außenwirtschaftsverordnung) came into effect. It specifies examples of critical industries that, due to their activity, run an enhanced risk of threating public order or security in Germany if acquired by a non-EU investor, and thus triggered a mandatory filing. For a large number of transactions involving non-EU buyers, this has resulted in increased discussion about whether or not a mandatory filing is necessary, whether to make a voluntary filing and whether there is a risk that the BMWi will block the transaction. At the end of 2018, media companies were added to the list of critical industries, and the shareholding threshold for transactions in certain sectors that may trigger a mandatory filing or review has been reduced from 25% to 10%.

Regulatory changes under discussion

The recent amendments to the German Foreign Trade and Payments Ordinance (Außenwirtschaftsverordnung) may have an impact on inbound M&A from non-EU investors. As the BMWi has a considerable amount of discretion regarding how to implement the new rules, it remains to be seen how disruptive the new rules will be and to what extent general political movements will try to influence the process. In any event, the mere filing requirement will add some uncertainty to affected transactions.

MARKET NORMS

One area that clients often do not pay enough attention to are the transitional services necessary to operate the business after closing an M&A transaction. In carve-out situations, clients usually focus on this area with sufficient diligence as the standalone abilities of the business is a key parameter. However, clients should also be aware of this issue in other M&A situations, and take the necessary steps to ensure that the business can operate post-closing without disruption.

PUBLIC M&A

The first important issue a bidder in a public takeover in Germany must understand is what "control" means. German public companies are usually organised as stock corporations (Aktiengesellschaften). Legally, stock corporations (and their day to day business) are independently run by their management board (Vorstand) which in turn is appointed and controlled by the supervisory board (Aufsichtsrat). Shareholders elect the members of the supervisory board by simple majority vote. Consequently, even with over 50% of the shares in a German public company, a shareholder only has indirect influence on its day-to-day business, particularly as neither the majority shareholder nor the supervisory board may give instructions to the management board. In order to do that, the shareholder would have to enter into a so-called control agreement (Beherrschungsvertrag) with the stock corporation which, amongst other protective mechanisms for minority shareholders, requires a 75% affirmative vote of the shareholders' meeting.

Thus, in order to safely obtain full control, a bidder must acquire 75% of the outstanding voting rights in the German public company. Recent years have shown that this threshold (and even 50%) is very hard to obtain in hostile scenarios and those hostile offers – unless they become friendly – have not been successful. The key factor to come to a friendly offer is to have a credible and convincing business story supporting the takeover to win over the target's management and a compelling offer price that reflects the real value of the target, its business potential and a premium to the current share price.

Conditions for a public takeover

Generally, the BaFin takes a rather restrictive position regarding offer conditions. Voluntary public takeover offers are usually subject to regulatory approvals, fairly standardised market- and company- MACs and no defensive measures (such as capital increases during the offer period) being taken. There is often a minimum acceptance threshold. Mandatory offers, ie those triggered by reaching a minimum 30% shareholding, can only be subject to regulatory conditions.

Break fees

Break fees are very rare in German public takeovers and thus, no real market standard exists.

PRIVATE M&A

In the current seller-friendly German market, locked-box is the predominantly used mechanism. Warranty and indemnity (W&I) insurance, which was rather uncommon in the German market a few years ago, is now probably an accepted instrument.

Conditions for a private takeover

Regulatory conditions, including merger control, are widely accepted (and where applicable pretty much mandatory). MAC or bring-down conditions are fairly rare in the currently seller-friendly market. Other conditions are usually deal-specific.

Foreign governing law

Deals for German assets or shares are usually governed by German law.

The exit environment

2018 was an excellent year for exits in Germany, both for trade sales and IPOs. IPOs were fuelled by the record high valuations on the German stock market. Trade sales (to financial sponsors as well as to strategic investors) resulted in high valuations and very seller friendly terms, with financial sponsors eager to invest capital driving the competition.

OUTLOOK

German corporates and financial sponsors seem to expect at least stable M&A activity for the next 6-12 months. The monetary policy of the European Central Bank to keep interest rates at their low levels supports this expectation. However, market participants should closely monitor the general economic environment. The second half of 2019 may also show the impact of Brexit.

About the author |

||

|

|

Dr Markus Lauer Partner, Herbert Smith Freehills Germany Frankfurt am Main, Germany T: +49 69 2222 82435 F: +49 69 2222 82499 W: www.herbertsmithfreehills.com For more than 15 years, Markus Lauer has been assisting industrial clients, private equity houses and financial institutions in public takeovers, private M&A, private equity, joint-ventures and capital markets. Recently, Markus advised in some of the most prominent public M&A transactions in the German market, involving Grammer, Ningbo Jifeng, Vonovia, Deutsche Wohnen, GSW, GAGFAH, Italmobiliare, HeidelbergCement, KUKA, Industrial and Commercial Bank of China, LSE, Deutsche Börse, Goldman Sachs, McKesson, Barclays and UBS. |

About the author |

||

|

|

Dr Nico Abel Partner, Herbert Smith Freehills Germany Frankfurt am Main, Germany T: +49 69 2222 82430 F: +49 69 2222 82499 W: www.herbertsmithfreehills.com Nico Abel has more than 20 years' experience advising corporates, financial investors and financial institutions on international mergers and acquisitions, including private acquisitions and disposals, public takeovers, joint-ventures and restructurings. His recent experience includes transactions in the financial services, energy, infrastructure and transport sectors. |